Completed Contract Method or CCM is one of the accounting methods used in the construction industry to recognize revenue and expenses after the work completes. This is a method to simplify the accounting process of construction projects.

For most contractors in The Philippines, they usually used this method for short-term or uncertain projects where estimating costs can be difficult. This article will help you to optimize the usage of Completed Contract Method.

- Completed Contract Method (CCM) is an accounting method that recognizes project revenue and profit only after construction work is fully completed.

- Contractors commonly use CCM for short-term or uncertain projects where costs, timelines, and project scopes are difficult to estimate accurately.

- Under certain conditions, CCM can still comply with GAAP and Philippine accounting regulations, including PFRS and BIR reporting requirements.

- ScaleOcean Construction Accounting ERP Software helps construction companies improve cost tracking, invoicing, and project management in one system.

1. What is the Complete Contract Method?

The Completed Contract Method (CCM) is an accounting method to record revenue and profit after a project is done. This method focuses on calculating the expenses after the work is done, even if the client has already paid part of the money.

Usually, contractors use this method for short-term or projects with uncertainties such as fluctuating costs, delays, changing scopes. Using CCM can avoid recognizing revenue too early before the final costs of the project are clear.

Compared to other accounting methods, CCM provides a simpler way to recognize income because financial results are reported once the project is finished. However, businesses still need proper documentation to support project reporting.

2. How does the Complete Contract Method (CCM) Work?

The construction billing process may be difficult to understand because it requires a lot of compliance and tax regulations. However, several projects may use CCM to simplify the process. Here some Complete Contract Method process usually includes:

- Recording Project Costs: Usually, construction companies record labor, materials, and subcontractor expenses during project execution. These costs are temporarily stored under work-in-progress accounts.

- Delaying Revenue Recognition: Even if contractors receive partial payments from clients, the revenue is not officially recognized yet. Payments received are usually recorded as liabilities or deferred income until project completion.

- Recognizing Revenue After Completion: Once the project is completed, the contractor records the entire project revenue and expenses in the financial statements. Then, profit or loss is calculated based on the total project performance.

The methods above are often associated with proper project tracking and accurate construction accounting practices to ensure all project costs are documented correctly before final reporting.

3. When Should the Complete Contract Method be Used?

When trying to use CCM, project managers should be careful because it is not suitable for every project. This method is typically used under specific situations where the outcomes are difficult to estimate. Here some common situations of applying CCM:

- Short-Term Construction Projects: First, common situations that applying CCM are projects that can be completed within a short period, for example like small renovations or residential construction projects.

- Projects with Uncertain Costs: Second, if project costs or timelines are difficult to estimate due to changing prices or design revisions, contractors may prefer CCM to avoid inaccurate revenue.

- High-Risk Contracts: Not only difficult estimating cost, projects with potential disputes, delays, or uncertain payment usually apply to CCM because contractors only recognize revenue after completion.

- Simpler Reporting: Another well-known situation of applying CCM is when some smaller contractors want simple and easy financial reporting.

In addition, contractors also combine proper project monitoring systems and construction accounting software to improve cost tracking and financial accuracy during project execution.

4. Pros and Cons of Complete Contract Method

Like other accounting methods, the Completed Contract Method offers several advantages and disadvantages for construction businesses. Here are some pros and contras of applying CCM method in financial flows.

a. Advantages of CCM

Completed Contract Method is one of the payment methods that offers several advantages for managing cash flow and project expenses effectively. Here are some advantages of applying this method in construction projects:

- Simpler Financial Reporting: One of the main benefits of CCM is it serves simple report documents of construction billing. Companies do not need to estimate project completion percentages regularly, which reduces administrative complexity.

- Reduced Estimation Errors: Since revenue is recognized only after a project is done, contractors can prevent inaccurate profit estimates caused by fluctuating project costs.

- Useful for Uncertain Projects: In addition, CCM also works well for projects with unpredictable timelines or changing project scopes.

b. Disadvantages of CCM

Although the Completed Contract Method offers several advantages, there are also some downsides to applying this method in construction projects. Here are some disadvantages of CCM:

- Delayed Profit Recognition: Because CCM requesting payment after the work’s done, businesses may appear less profitable during project execution because revenue is postponed until completion.

- Uneven Financial Statements: Although it simplifies expense records, the downside of CCM is making financial reports seem to fluctuate. It is because revenues are recognized all at once after project completion.

- Potential Tax Implications: Delaying revenue recognition may impact tax calculations depending on local accounting and taxation regulations in the Philippines.

Because of these challenges, contractors often need better project cash flow management, especially when handling billing in construction processes and project payment schedules.

5. Completed Contract Method vs. Percentage of Completion Method

The Completed Contract Method and Percentage of Completion Method are two common accounting approaches used in construction projects. However, both methods differ in how they recognize revenue and expenses. Here are the differences:

| Aspect | Completed Contract Method | Percentage of Completion Method |

|---|---|---|

| Revenue Recognition | After project completion | Gradually during project progress |

| Financial Reporting | Simpler | More detailed and continuous |

| Profit Visibility | Delayed until project completion | Recognized progressively |

| Suitable for | Short-term or uncertain projects | Long-term predictable projects |

6. Is Completed Contract Method GAAP Compliant?

Many contractors often ask, “Is Completed Contract Method GAAP compliant?” The answer is yes, but only under certain conditions. Under Generally Accepted Accounting Principles (GAAP), CCM can still be used when project estimation cannot be measured.

However, accounting standards generally prefer methods that recognize revenue progressively during working time. It is because contractors can maintain financial flows regularly and spend expenses on other important costs.

In the Philippines, contractors should comply with local accounting regulations which is Philippine Financial Reporting Standards (PFRS). It follows international principles, thus companies are encouraged to use methods that accurately reflect progress.

Not only standard principle, companies also must consider tax reporting requirements from the Bureau of Internal Revenue (BIR). Choosing the right accounting method helps businesses maintain accurate financial statements and improve compliance.

Also, not only compliance, companies who are handling project retention payments or retainage should maintain accurate records to avoid reporting discrepancies at project completion.

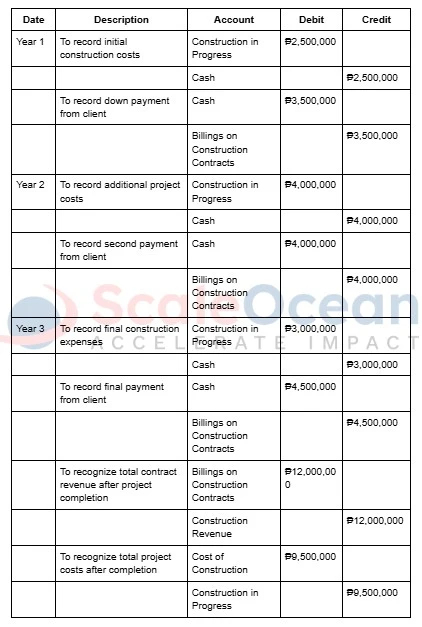

7. Example of Completed Contract Method in the Philippines

To better understand the Completed Contract Method in actual accounting practices, Here is the example of how this financial method to applied to a short-term project in the Philippines:

Suppose a construction company receives a contract worth ₱12,000,000 to build a two-story office building. Under the CCM, the company records construction costs during the project but recognizes revenue after the project is completed.

CCM Example Journal Entry

8. In Conclusion

The Completed Contract Method or also known as CCM is an accounting approach that recognizes project revenue after the project is completed. Generally, this method is used for short-term or uncertain projects to reduce estimation risks.

However, businesses should also consider its limitations, including delayed profit and uneven financial statements. Choosing the right accounting method depends on project complexity and compliance requirements in the Philippines.

To improve accounting accuracy, and financial visibility, construction companies can use ScaleOcean Construction Accounting ERP Software. The system helps contractors manage project costs, invoicing, and operational workflows efficiently in one system.

If you want to simplify construction accounting, you can also request a free demo to explore how the system supports your construction business operations.

FAQ:

1. How does the completed contract method work?

CCM records all project revenue and costs only after the contract is fully completed, not during the project timeline.

2. What is the difference between CCM and POC method?

POC recognizes revenue gradually as work progresses, while CCM records revenue only after the project is completed.

3. Can you use the completed contract method for GAAP?

Yes, CCM is allowed under US GAAP, but ASC 606 limits its use to certain contract situations.