When a company operates without a Profit and Loss statement, it’s similar to flying an airplane blind through a raging storm.

Without it, there’s a higher risk of missing hidden costs, using up cash reserves, and even going out of business, because there are no early signs to alert business owners to a problem.

This financial statement is known as the heartbeat of the financials, as it clearly demonstrates the business’s bottom line. It also aids in tracking profitability, gaining investors’ confidence, and optimizing business taxes while keeping the company viable for growth.

As it plays such a vital role, the article below will go over what a P&L statement is, the various parts of a Profit and Loss Statement including revenue, gross profit, and operating income, and more importantly, why businesses must conduct regular analysis of these key parts to improve financial management and decision-making for increased operational performance and growth.

- A Profit and Loss (P&L) statement is a crucial financial document that summarizes a company’s revenues, costs, and profits over a given period, providing insights into its financial health.

- Key components of the P&L statement, such as revenue, COGS, gross profit, and operating expenses, help businesses evaluate their financial performance and identify areas for improvement.

- The types of P&L statements, including single-step and multi-step formats, offer different levels of detail to suit the complexity of a business’s financial needs.

- ScaleOcean’s accounting software simplifies P&L analysis by automating data recording, offering real-time insights, and streamlining financial reporting, which enhances decision-making and operational efficiency.

What is a Profit and Loss (P&L) Statement?

A Profit and Loss Statement (P&L) or an income statement is an important financial statement that details a company’s income, expenditures, and spending throughout a specified period.

This document gives substantial information to the audience as to how profitable a business is, as this statement primarily takes into account the increasing sales of the business.

Essentially, it gives a snapshot of the company’s financial performance, often over a fiscal quarter or fiscal year, and it is used by businesses, investors, and stakeholders in Singapore to assess the company’s financial health and effectiveness.

For the retail or manufacturing industries, the statement is a pivotal document as it gives insight into the business’s financial performance, which in turn will aid business owners to improve performance.

The rapidly changing Singapore market requires companies to keep track of their expenditures and increase profitability; the P&L has been a crucial statement for management.

How Do P&L Statements Work?

The Profit and Loss (P&L) Statement is considered to be one of the three core financial statements, along with the cash flow statements and the balance sheets, which collectively present a company’s complete financial condition.

P&L specifically outlines the revenue and expenses over the entire duration, where we take a look into how a P&L statement is formulated. Here, we will take a closer look at the Profit and Loss statement formula and what it tells us about a company’s financials:

P&L Statements Formula

The profit and loss statement formula is critical as it determines the company’s net income. This statement accounts for business revenues, expenditures, as well as non-operational aspects like gains and losses to generate a picture of how profitable the business is during the particular period.

The formula for the P&L statement is:

Net Income = Revenue – Expenses + Gains – Losses

To work out this formula, you’ll need the revenues of the company, which includes all income from sales; the costs, or rather expenses, are any costs incurred to run the business (rent, utilities, employee wages), while losses and losses are costs or profits incurred due to activities not in line with the normal day-to-day operations of the business.

If, for example, a company generated $1,000,000 in revenue and $600,000 in expenditures, $50,000 in gains, and $20,000 in losses. Plugging these values into the formula, we get:

Net Income = $1,000,000 – $600,000 + $50,000 – $20,000

Calculating the outcome gives us $430,000, which signifies that the company has made $430,000 in profits after all expenses, income, and non-operating factors were accounted for during the particular period.

What the Profit and Loss (P&L) Statement Reveals

Once the formula has been applied, the profit and loss statement signifies the outcome of a company’s business activity during a certain period.

The net income derived through the formula indicates the company’s overall profitability after taking all expenses, revenues, and other sources of income into account. Beyond just profitability, the P&L also demonstrates the efficiency with which the company is functioning.

The outcome of the calculation in the example shown above demonstrates that a net income of $430,000 indicates a highly efficient company, as it has made a profit that exceeds its operating expenses and other external revenue or losses.

Lastly, business owners, investors, and stakeholders will be able to see the trend of the company’s profitability and, if calculations have been conducted well, would know what to improve (increase revenue or minimize spending) to ensure future growth of the business.

Key Components of a P&L Statement

The P&L Statement includes various important components that aid in a company’s comprehensive evaluation and understanding of its financial performance.

These components enable an organization to easily interpret its profits and losses from a functional aspect. The critical components included in a P&L Statement are listed below:

- Cost of Goods & Services (COGS): This term describes the cost of goods and/or services directly attributable to the production/delivery.

- Gross Income: This term explains the business’s profit before taking any expenses such as overheads and taxes into account. Revenue- COGS= Gross Income

- Revenue: Referred to as the ‘top line’, revenue describes the amount of income received from primary business activities and product sales.

- Operating Income: This is a profit calculated after deducting the total operating expenses from the business’s gross income.

- Operating Expenses: This indicates the daily running costs of a business, which are separate to any products being produced or service being delivered e.g., Wages, rent, and marketing.

- Miscellaneous Expenses: Costs which are outside the regular operations of the business e.g. Unusual administrative costs and one-off legal charges.

- Earnings Per Share (EPS): A performance indicator used in businesses that details a company’s profit allocation for each of its common shares.

- EBT (Earnings Before Taxes): This is a measurement of a company’s financial performance calculated after subtracting total expenses, excluding income tax, from revenue.

- Net Income: The ‘bottom line’, net income represents a company’s total profit after the cost of expenses, interest, taxes, etc have been met.

Methods for Preparing a P&L Statement

The method in which a company produces a Profit and Loss statement is dependent on the business’s structure or requirements.

Also, there are two fundamental ways of preparing the document, which are the cash basis method and the accrual basis method, which have different interpretations for revenue and expense recognition:

Cash Basis

When using the cash basis method, revenues and expenses are only recognized once they have actually been exchanged or transferred. In other words, revenue is recognized when it is received and expenses when paid.

This type of reporting is generally easier to monitor, as cash receipts and expenditures are recorded at the time of the transaction and hence is popular with small businesses orsole-traders who use this reporting method in order to track cash efficiently.

Although cash-based reporting is a simpler way of keeping tabs on business transactions, it may be misleading during the duration between the transfer of funds or sale; hence, larger companies tend not to use this method for reporting purposes.

Accrual Basis

The accrual method of accounting recognizes income as earned and expenses as incurred, not when they are paid. This type of accounting helps a company get a truer picture of its position because it records both current and all revenue and expenses during the accounting period.

The accrual method is required by GAAP for larger companies and presents the business as having more assets and liabilities because it shows receivables and payables.

Types of P&L Statements

The Profit and Loss (P&L) statement can be presented in various formats, depending on the complexity of the business’s financials and the level of detail required. These formats help businesses present their financial data in a way that suits their specific operational needs.

It is important to understand the types of P&L statements to determine which is most suitable for your business. Here are the main types of P&L statements:

- Single-Step Income Statement: In this simple format, only one subtotal is used for all revenues and another one for all expenses. Although simple to read, it is not detailed enough for detailed operational analysis, which is important in the accrual accounting process.

- Multi-Step Income Statement: This is a more detailed report that separates revenue and expenses that arise from operating activities from those that arise from non-operating activities. It computes the Gross Profit and Operating Income to allow for better observation of efficiency.

- Condensed P&L Statements: This is a high-level summary of accounts. Line items are summarized into wider categories to display key figures to an executive or external stakeholder, instead of having to wade through the less relevant data.

- Common-size Statements: This is a specialized report in which every line item is shown as a percentage of total sales. This allows easy comparison across business sizes.

Importance of the P&L Statement

The Profit and Loss (P&L) statement is a vital financial document that outlines a company’s financial performance. It is used by businesses, investors, and other stakeholders to evaluate profitability, operational efficiency, and overall financial health.

The profit and loss statement plays a critical role in strategic decision-making because it provides a clear picture of a business’s sales, costs, and profits. The significance of the P&L statement can be identified in the following areas:

Financial Performance Assessment

The P&L statement is key to determining a business’s profitability and operational efficiency. Through the revenue and costs analysis of this statement, a company can identify whether it is generating enough revenue to cover its expenses and still grow.

Understanding the difference between bookkeeping and accounting will further ensure that the data feeding the P&L statement is accurate and correctly classified.

A well-kept profit and loss statement will help a company identify cost-saving or revenue-generating opportunities, thus making it an indispensable performance assessment tool.

Decision-Making Tool

The P&L statement is a crucial tool to be used by management for decision-making processes. The statement provides a wealth of information essential for budgeting, forecasting, and strategy formulation.

A critical analysis of the statement will enable managers to adjust strategies to optimize profitability, efficiently allocate resources, and produce more reliable financial forecasts for the future.

Investor Relations

The P&L statement offers a clear presentation of financial health to investors and shareholders.

By offering a detailed record of revenues and costs incurred by a business, investors will be better able to analyze the potential risk and return on investment.

A strong P&L report builds confidence, which is important for attracting and retaining investors.

Compliance and Reporting

Reporting to external parties or government is an important component of the P&L statement. Companies in Singapore are required to file their P&L statement to satisfy their tax requirements and to ensure that they meet regulatory guidelines.

According to the data we found from IRAS, sole proprietors in Singapore are to provide either a 2-Line or 4-Line Statement to declare their income. If the revenue is above $200,000, a 4-Line Statement should be filed.

By submitting accurate P&L reports, it ensures a business stays compliant and maintains positive relationships with the authorities and investors.

Limitations of the P&L Statement

While the Profit and Loss (P&L) statement is a key financial document, its limitations should be considered when assessing the financial condition of a business.

The limits of the P&L are derived from the fact that it only focuses on operating success and profitability without taking into account other vital aspects of the finances.

Recognizing these limits is important in a comprehensive analysis of the financial condition of a business. The fundamental limitations of the profit and loss statement are:

- Non-Cash Items: The P&L indicates profitability but does not take actual cash available into account. Such items like depreciation will be considered part of profit but are not actual cash flowing into the business, which is critical for operating purposes.

- Historical Data: This statement only covers previous periods and doesn’t cover changes in market trends. It reflects a look rather than a forecast for the future.

- Ignores Non-Operating Factors: By accounting only for revenue and expenses incurred, the bigger picture is ignored, including components like assets, liabilities, and equity. A balance sheet is needed for a complete financial picture.

Analyzing a P&L Statement

Analyzing the Profit and Loss (P&L) statement is vital for a business and investors in understanding its financial performance and for making wise business decisions.

The P&L statement allows you to identify a business’s profit, analyze it over time, and diagnose problematic areas. By carefully examining the statement, the key areas of analysis are as follows:

1. Key Metrics

Key P&L metrics give you a clear and succinct method to evaluate the profitability and efficiency of a business. These indicators demonstrate how efficiently a business is capable of producing profits from its revenues and managing costs at different points of its operation.

Key performance indicators to assess in the P&L statement are:

Gross Profit Margin

This key metric is used to measure how well a business produces and sells its products in relation to its revenues. It is used to measure the production cost-related figures of the business and understand how much profit is available to cover the costs of operations.

The formula to calculate gross profit margin is:

Gross Profit Margin = Gross Profit / Revenue

This formula will indicate what percentage of revenue surpasses the COGS, representing how efficiently a business controls its production costs.

A high gross profit margin will indicate a successful business capable of controlling production expenses while retaining significant profits.

Operating Profit Margin

This metric indicates the overall profit of a business, excluding all other income and expenses like interest payments or tax charges, thereby showing how well a business generates profits from its core activities.

A look at the operating profit margin is essential in showing the efficiency a business is capable of converting revenue into operating profit. It is calculated as:

Operating Profit Margin = Operating Income / Revenue

This formula is able to calculate what percentage of the revenues are available to cover operational expenses after deducting operational costs.

High operating profit margins generally indicate that the business is profitable and efficient in turning revenues into operating profit.

Net Profit Margin

The net profit margin measures a business’s total profit after all expenses, including operational costs, interest, and tax, have been accounted for. It provides a view on the profitability of a business after the deduction of all the costs associated with its operations. The formula is as follows:

Net Profit Margin = Net Income / Revenue

This will indicate the percentage of revenues converted to pure profit after all costs. A larger net profit margin shows that the company is efficiently transforming revenue into profit, indicating good financial health.

2. Trend Analysis

Trend analysis looks at profit and loss statements over multiple periods and trends in revenue, expenses, and profits.

The data that this type of analysis uses comes from reliable double-entry accounting information, and it is this that enables companies to find trends, predict their business performance, and correct the problem of increasing costs or falling sales.

3. Industry Comparison

Industry comparison refers to comparing a firm’s performance against the average for that particular industry or competing firms.

The advantage to a company is to assess how they fare against the competitors so they know their positioning in relation to rivals and areas they need to improve in to compete.

P&L Management

Successful P&L management is managing both expenses and income. Profit and loss must be watched consistently to make prudent decision which would lead the business to profit and sustainability. The effective strategies are:

- Controlling Costs: This means cutting wasteful spending and utilizing resources efficiently. Studying the general ledger will help cut expenses without compromising product quality or key business operations.

- Increasing revenue: This involves increasing sales either by expanding into new markets or improving pricing strategies. Identifying these opportunities clearly increases the bottom line and prospects.

- Increasing efficiency: The process of making business operations more efficient through work streamlining and automation would increase productivity and profit margins without necessarily requiring an increase in the sales of the business.

P&L in the Singapore Context

In the Singapore context, the Profit and Loss statement plays an integral role in the financial reporting process of a firm.

This statement helps to identify a company’s financial performance, and the preparation of this document is legally required by laws and regulations to allow the parties to review the company’s financial health.

As such, companies must follow the proper procedures to allow the accurate and compliant reporting of financial performance. Here are the aspects of a profit and loss in Singapore:

Regulatory Requirements

Firms in Singapore are mandated to prepare and submit the financial statement, which also includes the Profit and Loss account, as part of their annual statutory reporting obligations.

It helps to enhance transparency and provides users with an overall view of the firm’s financial status. It has to be filed with ACRA & IRAS and be audited to ensure the authenticity of the report.

Tax Implications

It calculates and sums up the net profit or loss of the company, and this would be used for calculating its tax payable amount for the purpose of taxing business in Singapore.

Recording of income and expenses accurately is needed to properly compute tax on business, and in order to prevent any penalty for inaccurate reporting of the statement of accounts, accurate recording must be performed at the beginning.

In addition to this, understanding the definition of expenses and tax reliefs will also help to cut tax.

Compliance Standards

A company that needs to prepare a profit and loss statement account in Singapore must abide by the Singapore Financial Reporting Standards (SFRS).

With the standardization in the SFRS, which outlines reporting norms of income, expense recognition, and reporting and presentation, businesses are guaranteed transparency and consistency.

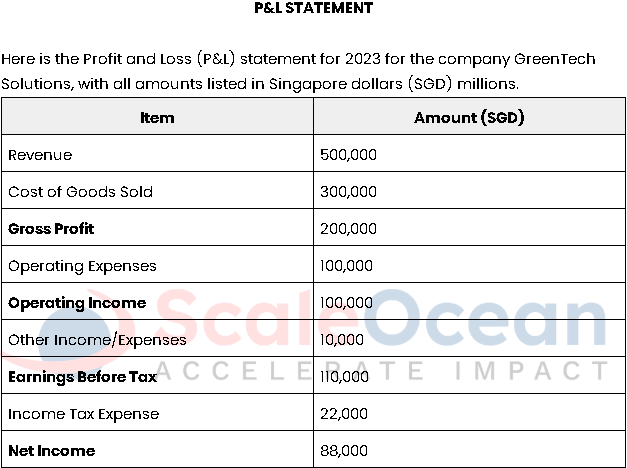

Practical Application: P&L Statement Example

The statement below of the Profit & Loss (P&L) shows a P&L for the financial year ending 2023 by GreenTech Solutions (in Million SGD). For the year, the income was SGD 500,000, and COGS amounted to SGD 300,000 for a Gross profit of SGD 200,000.

Operating profit for the year, after deducting expenses of SGD 100,000, is SGD 100,000. For the year, profit before tax was SGD 110,000 after other income/expenses of SGD 10,000.

After Income tax expense of SGD 22,000, the Net Profit of SGD 88,000 resulted in final reporting. Below is an example of the statement to be prepared:

Streamline Your P&L Analysis with ScaleOcean’s Accounting Software

With its easy interface, companies in Singapore can automate the entire financial process with ScaleOcean. It integrates with sales, purchasing, inventory, and asset management and helps in keeping track of all the financial information in real time.

This ensures you are provided with the exact current status of the company, hence reducing risks.

It ensures automatic logging and maintenance of all transaction entries and reports, thereby generating real-time information that can also be used in management to aid in quick and smart decision-making processes, especially by start-ups in Singapore and to achieve rapid growth.

Feel free to visit ScaleOcean’s website if you are interested in knowing more or availing a free demo of the accounting software so that you may check it for yourself if it helps in improving your financial accounting processes.

A CTC grant is also available to support Singaporean companies with the initial setup cost. The main features of ScaleOcean are:

- End-to-End Financial Integration: ScaleOcean’s accounting integrates with sales, procurement, inventory, and asset management for real-time financial tracking.

- Comprehensive Financial Reporting: Provides customizable Profit & Loss, balance sheets, and cash flow reports for quick financial insights.

- Automated Transaction Recording: Automatically records transactions like sales, purchases, and inventory adjustments, reducing errors.

- Real-Time Budget Comparison: Compares actual P&L figures with budgeted ones in real-time for better financial oversight.

- Seamless Integration Across Modules: Accounting integrates smoothly with other ScaleOcean modules like sales, inventory, and procurement.

Conclusion

The profit and loss (P&L) statement is an important financial record, used in financial accounting to measure a company’s ability to generate revenue through its operations. Summarizing revenues, expenses, costs, and gains or losses on disposal of assets.

It reports the net profit or loss of a company for a specified period of time. Businesses can look back and monitor performance over time, identify growth opportunities, and analyze it well by preparing a profit and loss statement on a regular interval.

It is one of the basic requirements of good accounting practice to effectively prepare it to enable a business organization to track its profitability and increase productivity and operational efficiency by using it with ScaleOcean’s accounting software to prepare reports automatically.

Effectively helping them to make correct and effective decisions to maximize the utilization of business resources and fulfill financial goals.

FAQ:

1. Can a P&L show a loss?

Yes, a P&L statement can show a loss. It lists what came in (revenue) and what went out (expenses), showing the remainder, which is net profit if positive, or net loss if negative. It’s the simplest way to determine if the business earned more than it spent.

2. Can I create a P&L in Excel?

Yes, you can create a P&L in Excel. It’s a simple and effective way to track your revenue, expenses, and net income. Excel allows you to easily organize and calculate numbers, making it a popular tool for businesses of all sizes.

3. How to explain P&L in an interview?

In an interview, explain the P&L statement as a key tool to assess profitability and financial health. It shows revenue, costs, and expenses, helping evaluate growth, decision-making, and financial performance for better business strategies.

4. How to create a profit or loss statement?

1. Collect revenue data: Gather all income generated from sales or services during the period.

2. Determine cost of goods sold (COGS): Calculate the direct costs associated with producing goods or services.

3. Calculate gross profit: Subtract COGS from total revenue to get gross profit.

4. Account for operating expenses: Include costs such as salaries, rent, utilities, and marketing.

5. Calculate operating income: Subtract operating expenses from gross profit to determine operating income.

6. Factor in other income/expenses: Add or subtract non-operating income or costs like investment gains or losses.

7. Subtract income tax: Calculate and subtract income tax to find the net income.

8. Organize the data: Use accounting software or a spreadsheet to display the information in an organized, clear manner.