Corporate tax in Singapore has played a significant role in establishing the country as a global business hub. With its strategic position, stable economy, and pro-business legislation, Singapore attracts companies looking for growth opportunities.

A key aspect contributing to this reputation is its competitive and open corporate tax system, designed to promote business expansion while remaining fiscally responsible.

According to World Bank data, Singapore’s Gross Domestic Product (GDP) will be roughly 501.43 billion USD in 2023, confirming its reputation as a high-income economy with a robust commercial sector.

In this article, we will dive into the key elements of corporate tax in Singapore, such as the corporate income tax rate, available tax exemptions, and incentives for businesses. We will also cover tax filing requirements, common mistakes, and how accounting software can streamline tax reporting and efficiency.

- For Singapore, the corporate income tax rate for firms locally formed or foreign corporations with activities in the nation is a flat corporate income tax rate of 17% on chargeable revenue.

- Key tax relief measures in Singapore include partial tax exemptions, start-up tax exemptions, and industry-specific incentives that reduce tax liabilities for businesses.

- Filing Obligations require businesses to submit ECI within three months after the fiscal year ends and Form C-S or C by November 30th to ensure compliance with IRAS and avoid penalties.

- ScaleOcean accounting software can improve tax management efficiency by automating calculations, tracking data in real-time, and ensuring full tax compliance.

Singapore Corporate Income Tax Rate

All firms in Singapore, whether locally formed or foreign corporations with activities in the nation, pay a flat corporate income tax rate of 17% on chargeable revenue. Unlike progressive tax regimes, this single-tier structure ensures that businesses only pay taxes on profits, with no additional charges on dividends paid to shareholders.

This competitive tax rate, along with Singapore’s large network of double taxation agreements (DTAs), makes the country an appealing choice for enterprises looking for tax savings.

Tax Exemptions and Incentives

Singapore offers a range of tax exemptions and incentives to support business growth, particularly for small enterprises, startups, and key industries. These schemes help reduce the overall tax burden, making it easier for businesses to reinvest in expansion, innovation, and operational improvements.

Below are some of the key tax relief measures available to companies in Singapore:

- Partial Tax Exemption (PTE): Singapore grants a partial tax exemption to SMEs. This exempts 75% of the first SGD 10,000 of chargeable income and 50% of the next SGD 190,000 from tax, resulting in a total exclusion of SGD 102,500 per year.

- Start-Up Tax Exemption (SUTE): Eligible startups receive a 75% exemption on the first SGD 100,000 of chargeable income and a 50% exemption on the next SGD 100,000 for the first three years of assessment, totaling an exempt income of SGD 125,000 per year.

- Industry-Specific Tax Incentives: Singapore offers tax breaks for businesses in industries like financial services, research and development, and worldwide trade, encouraging investment and innovation to enhance Singapore’s competitiveness globally.

- YA 2025 Tax Rebate: Businesses can benefit from a 50% rebate on their corporate tax payable, up to a maximum of SGD 40,000, with a guaranteed cash grant of at least SGD 2,000 for companies employing one or more local employees.

Filing Obligations

Businesses in Singapore must meet tight tax filing dates to maintain compliance with the Inland Revenue Authority of Singapore (IRAS). Companies must file crucial tax documents, such as an Estimated Chargeable Income (ECI) declaration, yearly tax returns, and tax invoice records, within specified times.

Timely and accurate filing not only avoids penalties but also helps firms retain good standing with tax authorities. The following are the main tax filing requirements for Singapore firms:

Estimated Chargeable Income (ECI)

Companies must submit an ECI to IRAS within three months after the end of their fiscal year. The ECI is an estimate of the company’s taxable income for the year that helps IRAS determine the company’s projected tax obligations.

Even if a corporation has no chargeable income, it must file the ECI unless specifically exempted. Businesses that file their corporate taxes early might take advantage of installment payment alternatives.

Form C-S/Form C Filing

Every year, corporations must submit Form C-S or Form C by November 30th to indicate their actual income for the year of assessment. Form C-S is a reduced form offered to small businesses that meet certain conditions, which reduces the reporting load.

Form C is the regular form required by larger businesses or those who do not qualify for Form C-S. To avoid penalties and compliance difficulties, ensure that you submit the correct form with accurate financial data.

Record-Keeping Requirements

In Singapore, businesses are required to keep clear and accurate financial records to meet tax regulations and simplify audits. This includes retaining important documents such as invoices, receipts, bank statements, and detailed accounting records.

All records must be kept for at least five years after the relevant Year of Assessment (YA), even if the business is no longer active. Having proper documentation helps ensure accurate tax filings and supports claims for deductions during audits.

If businesses fail to maintain accurate records, they may face penalties or complications during tax audits conducted by the Inland Revenue Authority of Singapore (IRAS). It is essential to comply with these record-keeping requirements.

Role of the Inland Revenue Authority of Singapore (IRAS) in Tax Compliance

The Inland Revenue Authority of Singapore (IRAS) plays a key role in ensuring businesses comply with tax regulations. It is responsible for enforcing corporate tax laws, conducting tax audits, and implementing penalties for businesses that do not follow the rules.

IRAS also supports businesses by offering useful resources, workshops, and clear guidelines to help them understand their tax obligations. With these tools, businesses can navigate the tax process more confidently and avoid mistakes.

To make things easier, IRAS provides digital services, such as e-filing systems. These tools allow businesses to file tax returns, make payments, and access tax-related information quickly and conveniently, ensuring a fair and transparent tax system.

Importance of Accounting Software in Tax Management

In a business, accounting software is needed to make the task of tax handling easier. It streamlines the tax calculation, reporting, and tracking process, minimizing errors and compliance risks in line with local tax laws. Businesses can easily keep pace with their tax duties with the right tools and can achieve HR KPI examples.

A few benefits that accounting software provides when it comes to taxation:

Automation of Tax Calculations

Accounting software can be used to help automate tax calculations to determine the correct tax rates, deductions, and exemptions based on Singapore’s corporate tax law. This decreases the likelihood of errors and noncompliance.

Further, automated tax functions assist firms in generating accurate tax paperwork and consistency throughout financial statements.

Integration with Financial Records

Integration with the financial records allows for up-to-date and accurate tax reporting. This saves on manual data input, reducing error probabilities and saving time.

Additionally, all relevant deductions can be easily recorded with the use of integrated accounting systems, including tracking of tax-deductible expenses, income generation, the use of payslip templates, and capital allowances, all of which will ensure that a firm is tracking all deductions that are eligible.

Real-Time Updates

By having up-to-date information regarding tax needs, companies can stay ahead of the tax deadline and prevent penalties. To guarantee HR compliance promptly, companies can arrange automated reminders for ECI files, Form C submission, and tax payments.

Additionally, tax forecasting tools allow businesses to have a fair idea of what it will require to pay in the future, based on current financial information.

Common Tax Filing Mistakes to Avoid

Filing corporate taxes correctly and on time is critical for Singapore businesses to avoid penalties and follow IRAS regulations. According to Singapore Incorporation Services, the Inland Revenue Authority of Singapore (IRAS) allows corporations between 11 and 22 months to file their corporate tax reports, depending on their accounting cycle.

However, many firms continue to make basic mistakes, such as missing deadlines or filing incorrectly, which can have serious financial and legal consequences. Here are the common risks to avoid:

Late Filing

Missing tax filing deadlines might result in financial penalties and enforcement measures by the IRS. Companies must submit their Estimated Chargeable Income (ECI) within three months of the end of the fiscal year, as well as Form C-S or Form C, by November 30 of each year.

Late files can result in fines and interrupt business operations, so it’s critical to set reminders or use accounting software for automated deadline tracking.

Inaccurate Reporting

Wrong numbers on a tax form might cause trouble later, when total numbers are off, or money earned goes unreported, problems will follow. Staying clear of fines means showing every dollar made, and leaving things out draws attention nobody wants.

Accurate reporting protects against costly mistakes, and careful reporting avoids extra fees down the road. Before submitting financial statements, companies can improve their human resource management process by considering using professional accounting services or tax software to ensure their accuracy.

Non-Compliance with Record-Keeping

From the moment a business files its taxes, it must hang on to every receipt, ledger entry, and report for five full years under Singapore rules; should inspectors come calling, missing documents might mean trouble, and penalties often follow.

Records aren’t just paperwork; they’re proof, kept ready long after submission. When records are kept neatly, whether online or on paper, companies can follow rules more easily. That way, vital money details never vanish when it matters most. In addition, a robust human resource strategy ensures that employee records, payroll data, and compliance with labor laws are effectively managed, supporting overall organizational efficiency.

What is the Process for Paying Corporate Tax in Singapore?

Corporate tax in Singapore is a straightforward and systematic process, starting with filing tax returns. The returns are to be filed on November 30th for any given year by the companies in Form C or Form C-S, which include information regarding their income and expenses.

Inland Revenue Authority of Singapore (IRAS) then checks the tax information submitted on the tax return and notifies the taxpayer with a Notice of Assessment (NOA). This will explain to businesses the amount of tax they are due, and they pay within 1 month of the NOA. There are several ways companies can make payments, including: GIRO, online banking, or a credit card.

For instance, a business with an outstanding debt of SGD 10,000 can easily pay the debt online if given the reference by IRAS. Payments and adherence to deadlines must be made on time in order to prevent the occurrence of extra fees. If, for example, the payments go over the deadline, late fees may be incurred, adding an unwanted burden to the financial situation of the company.

Strategies for Efficient Tax Reporting

Running an efficient business is crucial for the smooth reporting of taxes, as it will enable you to keep up with tax requirements and minimize tax liabilities. Adopting smart strategies, companies can steer clear of penalties and enhance financial results. Here are some helpful tips for improving your tax filing:

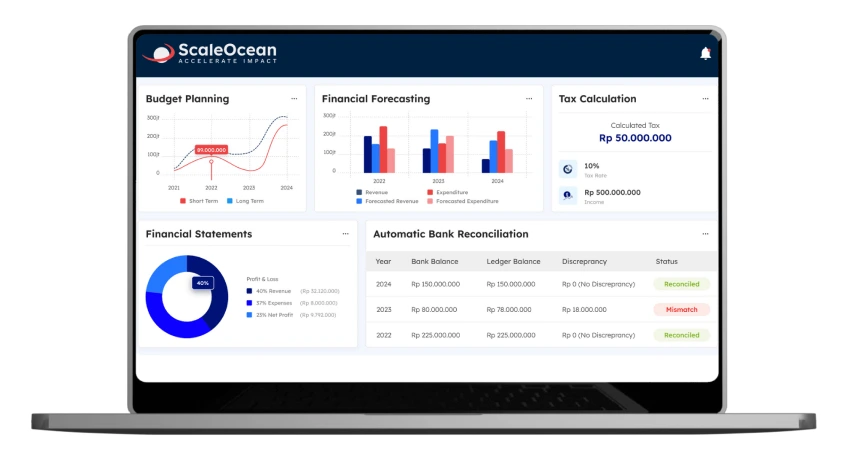

Leverage ScaleOcean Accounting Software for Tax Efficiency

With its scalable and affordable solution, businesses can save time on manual tasks and error-prone processing while managing corporate tax effectively, making tax management easier and more efficient. ScaleOcean accounting software streamlines the tax filing process, offering real-time automatic calculations, financial tracking, and seamless integration to make sure reporting is flawless and filings timely without breaking IRAS regulations.

There is a single platform that makes it easy for businesses to control their deductions, exemptions, and tax liabilities. Real-time insights from ScaleOcean minimize financial risks, boost cash circulation, and assist companies in tracking and dealing with the CTC grant with efficiency.

Businesses should explore a free demo to understand the advantages of making it automated and integrating seamlessly in real-time in order to boost their tax efficiency. Some advantages of the ScaleOcean accounting software are:

- Unlimited Users Without Additional Fees: Suitable for expanding businesses, allowing scaling up without paying an extra fee per user.

- All-in-One Solution With Comprehensive Modules: 200+ specific modules customized to fit your corporate needs, which take care to be consistent with financial operations when performing tax calculations.

- Flat and Transparent price: No hidden charges or fees make it a reliable alternative for midsize to enterprise businesses.

- Advanced Customization and Smart Configuration: Customers have the ability to customize dashboards and tax workflow to their own business tax structures and compliance requirements.

Maximize Tax Deductions

When minimizing your taxable income, be sure to maximize your allowable deductions, such as those related to employee salaries, employee training, travel expenses, and employee professional fees, among other expenses. These deductions will reduce your taxes and enhance cash flow.

Maintaining proper financial records is essential in helping to substantiate your claims and to prevent problems when audited. HR latest trends can also help identify areas where you can save costs and leverage tax-saving facilities.

Utilize Capital Allowances

Capital allowance can provide a tax treatment advantage by granting business relief for eligible items such as machinery, office furniture, nd vehicles. Thesereliefs enablee investment in productive assets and technology to sustain growth.

More than that, programmes such as Productivity and Innovation Credit (PIC) and Writing Down Allowance (WDA) encourage businesses to invest in technology and productivity equipment to help improve productivity in Singapore. Using them in the right way can decrease your taxes and help the growth strategy.

Engage Professional Tax Services

Singapore corporate tax rules might be complicated, particularly for firms with significant revenue generated or global transactions. Accredited tax professionals can help you ensure that your taxes are done correctly and that you take advantage of tax exemptions and deductions.

Tax specialists provide tax-related guidance on tax planning, compliance, and tax risks. In the same way that human resource planning ensures that companies do not miss Activities, having tax specialists helps ensure companies Do Not Miss Activities and maximise them for a durable and healthy enterprise, as well as their tax performance.

Conclusion

Any business must understand the Singapore corporate tax system to optimise tax benefits, minimise taxes, a nd comply with the IRAS regulatory requirements. Implementing measures like tax deductions, proper documentation, and forward-looking tax planning can help companies prevent such pitfalls as late submissions and errors.

With tax management, tax accounting software can ease the burden greatly; it is capable of real-time financial record keeping and can also integrate financial records, which automates the calculations of accounting for taxes. ScaleOcean’s accounting software streamlines the tax filing process, minimises tax filing errors, and guarantees adherence to Singapore’s tax regulations. Get a free demo today to see ScaleOcean’s benefits and features.

FAQ:

1. Are GST and corporate tax the same?

GST is an indirect tax applied to the supply of goods and services, while corporate tax is a direct tax imposed on a company’s profits. How these two taxes interact can either reduce or increase a business’s overall tax burden, depending on the planning strategies used.

2. Who is required to file corporate taxes?

Any business considered a taxable entity, including Free Zone entities, must register for corporate tax and obtain a registration number. In some cases, even businesses that are usually exempt may be required to register for corporate tax if asked by the Federal Tax Authority.

3. Who is exempt from corporation tax?

Typically, charities do not have to pay corporate or income tax. However, certain situations may require tax payments, especially when the charity engages in non-charitable activities or incurs expenses unrelated to its charitable purposes.

4. How much is the minimum corporate income tax?

The Minimum Corporate Income Tax (MCIT) is a 2% tax on gross income that applies starting from the fourth taxable year of business operations. Companies will pay whichever tax is higher: the regular corporate income tax or the MCIT.