A financial document that summarises all cash received and all cash spent in a specific period of time by a company is called a Cash Flow Statement. This makes it possible for organisations and stakeholders to understand and analyse the flow and usage of cash, a key aspect in operational efficiency, especially in competitive markets like Singapore.

A business must have a clear picture of its cash flow in order to ensure that on time, the payment is received, the operational requirements are met, and to have a good grasp of working capital. The statement also serves as a helpful tool to give a good idea about the company’s cash flow from its operating, investing, and financing activities.

Understanding and successfully managing cash flow is critical for sustaining growth and making sound financial decisions. With real-time insights into cash management, businesses can plan for future growth, invest in new opportunities, and maintain stability even during economic fluctuations.

- A cash flow statement is a key financial document that provides a comprehensive overview of a company’s cash inflows and outflows, helping businesses assess their financial performance over a specific period.

- There are two main methods for preparing a cash flow statement: the direct method, which categorizes cash receipts and payments, and the indirect method, which adjusts net income for changes in balance sheet items.

- The main components of a cash flow statement include net income, depreciation and amortization, changes in working capital, and investing and financing activities.

- Systems likeScaleOcean Accounting Software automate the creation of cash flow statements, improving efficiency and accuracy by integrating key financial data and reducing manual entry.

What Is a Cash Flow Statement?

A cash flow statement is one of the most important financial statements that businesses use to monitor their actual cash movements, offering a clear view of liquidity and its essential role in a company’s financial health.

Along with the income statement and balance sheet, it provides a comprehensive picture of the company’s cash inflows and outflows during a specific time period, helping to assess financial leverage and overall financial health.

This statement is critical for assessing a company’s liquidity, financial health, and ability to meet short-term obligations. It assists businesses, investors, and analysts in evaluating cash flow dynamics, ensuring that organizations can meet their current expenses without experiencing financial duress. The following are the primary components of a cash flow statement:

1. Operating Activities

Operating activities track the cash flow generated or used by a company’s normal day-to-day operations. This includes cash received from clients for sales and cash paid out for raw materials, wages, and other supplier costs, showing your business’s core financial performance.

These activities are critical for determining how well a company generates cash from its core business tasks, which affects its capacity to continue operations without external financing. The cash flow from operating activities is often compared with the profit and loss statement to assess how actual cash generation aligns with reported profitability.

2. Investing Activities

Investing activities involve cash flows from the purchase and sale of long-term assets used in a company’s operations. This includes all transactions involving property, plant, and equipment, as well as investments in securities or other businesses.

The general ledger is essential in accurately recording these transactions, ensuring that investments and asset purchases are properly tracked. The purpose of these actions is to help the company grow or adapt its asset base, which can have a substantial impact on future profitability and operations.

3. Financing Activities

Financing activities record the cash flows generated by a firm’s capital structure, which include cash flows resulting from borrowing and repaying loans, issuing stock, paying dividends to shareholders, etc. These are done to demonstrate the way in which a company generates value for its investors, alerting them to the direction in which the company is seeking to fund itself.

All companies that must cope with future financial requirements all need the cash flow statement. Tools like financial ERP software can help companies effortlessly evaluate and measure the flow of cash in the past so they can more accurately predict and budget for future expenses. They can have sufficient cash available to grow and run their business.

Why Is the Cash Flow Statement Important?

A cash flow statement allows investors, creditors, and Management to decide whether a firm has sufficient cash on hand and how it can utilise cash to run its business. This is useful for analysing liquidity, operational efficiencies, and investing decisions, and is a critical component of financial planning and forecasting future cash requirements.

Businesses in Singapore have to adhere to Singapore accounting standards to ensure the financial statements are accurate. According to ACRA Singapore, compliance with SFRS(I) allows entities to include a statement of compliance with the IFRS Accounting Standards in their first and subsequent SFRS(I) financial statements, providing transparency in their reporting.

The next section exemplifies some of the significance of a cash flow statement:

1. Liquidity Assessment

The cash flow statement is used to assess a company’s ability to meet its short-term demands. It shows the company has sufficient cash resources to operate for a while without borrowing any money and running a normal business.

2. Operational Efficiency

The cash flow statement shows the profitability of the company’s core activities by showing the amount of cash generated from the activities. Positive cash flow from operations indicates a strong and steady business plan, while negative cash flow could point to inefficiencies in need of a makeover.

A clear accrual accounting process will help companies better understand the timing differences between cash inflows and cash outflows, and expenses and revenues processed.

3. Investment Decisions

The cash flow statement helps investors analyse a company’s financial state and potential for growth. It gives a clearer picture of a company’s cash generation and cash usage, which has an impact on investment decisions such as buying this stock and/or extending financing.

4. Financial Planning

Companies need to use the cash flow statement to plan for future cash requirements. Using resources such as financial ERP software, companies have access to historical cash flows for review and can more accurately forecast and manage future cash flows.

The double-entry accounting process is optimised, with every transaction being accurately recorded and thus allowing visibility of financial health. This type of software can automate the financial data processing associated with planning for capital expenditures and also help companies enjoy adequate money to offer growth and functioning.

How to Prepare a Cash Flow Statement

To gain an understanding of the actual flow of cash within your business, it’s important to prepare a statement of cash flows. It enables simple tracking of cash inflows and outflows, giving valuable insight into the financial situation. There are several important steps in this approach:

1. Gather Financial Information

The first step to the cash flow statement is to gather the crucial financial information that will be needed to produce an accurate document. This includes net earnings, non-cash expenses such as depreciation, and changes in assets/liabilities from the balance sheet. Bank statements also provide valuable information about real cash transfer.

Disclosing accurate information is crucial to having a cash flow statement that accurately represents the company’s balance sheet. This information will be an important input to computing cash flows and being able to really see how business activities impact cash reserves over time.

2. Pick the Specific Procedure

There are two ways of creating a cash flow statement: the direct method and the indirect method. The indirect method begins with net income and incorporates any changes in non-cash items; the direct method shows the cash that comes in or goes out through operating activities.

The only choice made between these is whether you want to have the detail available or whether the company would prefer one. While the direct method provides a lot of detail about every cash transaction, the indirect method can be easier.

3. Calculate Cash Flow from Operating Activities

Operating activities are cash generated by the core business, such as cash received from customers and cash paid to suppliers. With the indirect method, you begin with the net income and add back working capital changes, such as the delta in accounts receivable and/or payable.

With the direct method, you just make a list of amounts of cash received from customers and cash paid out for expenses. Both approaches function very well to determine the actual cash flow generated or consumed from the company’s main operations, which is essential for its overall financial condition, particularly to determine the Net Present Value (NPV) of cash flows generated in the future.

4. Calculate Cash Flow from Investing Activities

Investing activities include the buying or selling of long-term assets (in this case, property or equipment). Giving a precise picture of the allocation of resources needed to grow the business, there is a record of cash spent on capital expenditures and cash received from asset sales.

These investment transactions can be used to assess the investments for future growth and the current cash position of businesses. Large sales might be the result of an increase in business, whereas large expenditures may signal repurposing of assets or a business transition.

5. Counting Cash Flow from Financing Activities

Financing activities include the purchase of financing, including raising capital, and the management of debt. This section monitors cash inflows of the issuing of stocks or borrowing of funds, and cash outflows of repaying debt, paying dividends and repurchasing stocks.

Funding behaviour knowledge assists companies in gauging their financing potential and the whole financial responsibilities. For instance, if borrowing is used for making instant cash, there is a possibility of affecting cash flows and profitability in the future, which is important to know.

6. Reconcile and Confirm the Cash Flow Statement

After calculating cash flows from operating, investing, and financing activities, you add them up to find the net change in cash. Reconciliation is then crucial, ensuring the statement perfectly aligns with the actual cash balance shown on your balance sheet.

Verifying the cash flow statement helps you quickly catch any discrepancies or mistakes. By carefully cross-checking the ending cash balance, businesses can ensure the statement accurately reflects the company’s cash position and confirm that the financial data is completely correct.

7. Review and Evaluate

Once the cash flow statement is done, it’s vital to assess any negative trends, which often signal financial issues. Reviewing your cash inflows and outflows offers valuable insight into the company’s ability to generate sufficient cash for all daily operations.

Furthermore, evaluating cash flow helps businesses see if they have enough liquidity to fund investments and meet financing obligations. Spotting unusual patterns or discrepancies allows for timely adjustments and better financial planning as you move forward.

Different Methods of Preparing a Cash Flow Statement

There are two main approaches for preparing a cash flow statement: direct and indirect. The direct technique categorizes important cash inflows and outflows while directly reporting cash receipts and payments. This method provides a detailed perspective of cash flows, allowing users to better understand the sources and uses of cash in daily operations, which is crucial for capital budgeting in project management, ensuring that projects are funded effectively and efficiently.

In contrast, the indirect technique begins with net income and adjusts for changes in balance sheet items to calculate cash flow from operating activities. This method is more generally employed because it simplifies the process by focusing on reconciling net income with cash flows, and it is frequently preferred since it relies on easily accessible financial data from the income statement and balance sheet.

So if you are curious what the specific differences are between direct and indirect methods, here is the table for it:

| Direct Method | Indirect Method |

|---|---|

|

|

Key Components Explained

The cash flow statement has several critical components that aid in understanding how a business manages its cash. These components indicate a variety of financial operations, including a company’s profitability and the impact of its investment and financing decisions. Businesses and investors can improve their understanding of a company’s cash management and financial health by evaluating these factors. The following are the main components, discussed in greater detail:

1. Net Income

Net income serves as the foundation of the cash flow statement, indicating a company’s profitability. Since it is derived from the income statement, it must comply with Singapore accounting standards to ensure accurate reflection of earnings. This ensures that all calculations, including adjustments for non-cash items, are in line with local regulations, providing stakeholders with a true and fair view of the company’s financial performance.

2. Depreciation and Amortization

Depreciation and amortization are non-cash charges that lower net income but have no direct impact on cash flow. These expenses reflect the gradual cost allocation of assets over their useful lives, often calculated using the depreciation formula. Depreciation and amortization are frequently brought back into operating cash flow on the cash flow statement because they do not entail actual cash withdrawals.

3. Changes in Working Capital

Working capital adjustments are made to account for changes in current assets and liabilities such as accounts receivable, payable, and inventories. These adjustments reflect a company’s short-term cash needs and aid in understanding how much cash is tied up or freed up in operations, which influences the overall cash flow position.

4. Investing and Financing Activities

Investing and financing operations show how a company’s decisions about investments and financing affect its financial position. This covers cash flows generated by the purchase or sale of long-term assets, as well as cash raised or spent in debt and equity transactions. These parts help evaluate the company’s financial strategy and resource allocation by demonstrating how cash is invested for future growth or refunded to stakeholders.

Interpreting the Cash Flow Statement

Understanding a company’s financial health requires the ability to interpret its cash flow statements. It provides information about how successfully a firm manages its cash and if it has enough funds to maintain operations, invest in growth, or return value to shareholders. The following sections illustrate how various types of cash flow might affect a company’s financial position:

1. Positive Cash Flow

When a corporation makes more cash than it uses, it indicates good financial health. Positive cash flow enables the company to reinvest in growth possibilities, reduce debt, or pay dividends to shareholders. It demonstrates the company’s capacity to run smoothly and sustain long-term profitability.

2. Negative Cash Flow

A negative cash flow may indicate that the company is aggressively investing in its future or that it is experiencing financial troubles. Negative cash flow may reflect a company’s growth phase, in which investment in assets and expansion outpace current cash generation, but it may also imply underlying profitability or liquidity difficulties if not managed appropriately.

3. Free Cash Flow

Free cash flow is the cash remaining after capital expenditures, indicating a company’s ability to reinvest in its operations, pay dividends, or pay down debt. This indicator is crucial for determining a company’s ability to manage its financial obligations and pursue new prospects without relying on external finance.

Common Pitfalls in Cash Flow Statements

Companies frequently encounter issues while preparing a cash flow statement, which can result in erroneous financial reporting. These problems can distort an understanding of a company’s genuine financial state, making it difficult for entrepreneurs and investors to make sound decisions. Here are some frequent pitfalls to avoid when evaluating a cash flow statement:

1. Overlooking Non-Cash Items

Failure to account for non-cash expenses, such as depreciation and amortization, can result in an erroneous cash flow analysis. Since these expenses diminish net income but have no effect on cash, failing to include them in the statement might misrepresent the underlying cash position, making the company appear less liquid than it is.

2. Misclassifying Cash Flows

Misclassifying cash flows can cause severe distortions in the financial picture. For example, identifying financing activities as operating cash flows or vice versa can mislead stakeholders about the company’s financial health, influencing decision-making and perhaps leading to misunderstandings regarding cash flow sources and uses.

3. Ignoring Seasonal Variations

Failure to account for seasonal swings in cash flow can lead to poor financial planning. Many organizations face cash flow peaks and troughs throughout the year owing to fluctuations in client demand or operational cycles. Ignoring these variations can result in an imbalance between cash inflows and outflows, potentially producing liquidity problems during off-peak periods.

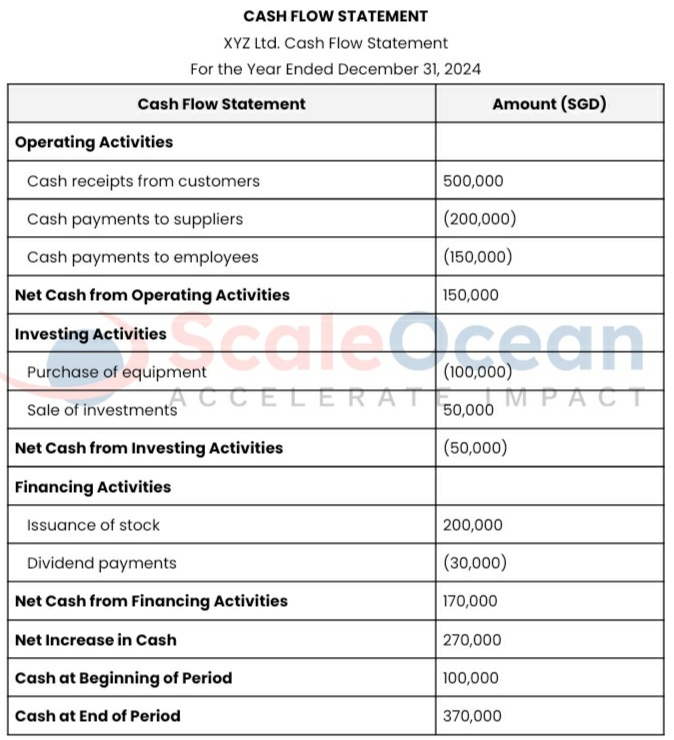

Example: Real-World Application

In this case study, XYZ Ltd. creates a cash flow statement that incorporates cash flows from operations, investments, and financing activities. Customer payments produce cash for the corporation, which then invests in new gear and raises capital through stock issuance and dividend payments. Analyzing these areas allows us to better understand how each activity affects the company’s cash condition. Below is an example of XYZ Ltd.’s cash flow statement that illustrates these activities in detail:

XYZ Ltd.’s operating activities show a strong cash inflow of SGD 500,000 from customer receipts, though cash outflows of SGD 200,000 to suppliers and SGD 150,000 to employees reduce the overall cash generated. Despite these outflows, the company maintains a positive net cash flow of SGD 150,000, indicating that its core operations are generating sufficient cash to support daily activities.

In investing and financing activities, the company shows a net cash outflow of SGD 50,000 from investments, indicating reinvestment in assets for future growth. Meanwhile, financing activities generated SGD 170,000 from stock issuance and dividend payments, reflecting successful capital raising and commitment to shareholder returns. Overall, XYZ Ltd. is financially stable, with sufficient liquidity for short-term obligations and growth.

According to the cash flow statement, XYZ Ltd. has a steady financial situation. Positive operating cash flow implies sufficient liquidity to meet short-term obligations, whereas negative investing cash flow indicates investment in future growth. The net positive cash flow from financing operations demonstrates effective capital raising. Overall, the company has adequate liquidity and financial flexibility to sustain operations and expansion.

Best Practices for Preparing a Cash Flow Statement

Creating an accurate and dependable cash flow statement is critical for good financial management. Following best practices ensures that the statement accurately represents the company’s true cash position and provides relevant information for decision-making. Here are some important principles to consider when creating a cash flow statement:

1. Regular Updates

The cash flow statement should be updated regularly to ensure it accurately reflects financial data. Regular updates enable organizations to analyze cash flows in real time, offering up-to-date liquidity insights and allowing for timely choices about cash management, investments, and financing requirements.

Reviewing these figures through clear bookkeeping and accounting reports also helps stakeholders understand how cash is moving through the business.

2. Accurate Classification

Cash flows must be properly classified into operating, investing, and financing activities to ensure accurate reporting. Misclassifying cash flows can distort the financial picture, making it harder to evaluate the company’s performance across all areas. Clear and accurate classification promotes transparency and improves decision-making based on reliable data.

3. Use of Accounting Software Like ScaleOcean

Accounting software, such as ScaleOcean, can help automate and streamline the preparation of financial statements, including the cash flow statement. These software solutions automate operations like data entry, categorization, and report generation, allowing businesses to save time, decrease human error, and ensure more accurate data.

Accounting software provides increased efficiency, real-time financial insights, better cash flow management, and simpler compliance with financial requirements. If you want to discover how it works for your business, ScaleOcean provides a free demo where you can try out its impressive features firsthand. Furthermore, firms may be eligible for the CTC Grant to help with the expense of implementing this software. ScaleOcean’s software includes the following major features:

- Unlimited Users at No Extra Cost: ScaleOcean allows unlimited users without additional charges, supporting business growth.

- All-in-One Solution: Offers over 200 modules, covering a wide range of business needs in one system.

- Industry-Specific Customization: Tailored solutions for various industries like manufacturing, retail, and F&B.

- Business Process Automation: Automates key operations, reducing human error and improving efficiency.

- Flat and Transparent Pricing: Offers clear, cost-effective pricing without hidden fees or surprise costs.

Conclusion

A cash flow statement is critical for ensuring financial transparency, providing stakeholders with a clear picture of a company’s cash position. It enables investors, creditors, and management to evaluate how efficiently a firm generates cash to meet its obligations and fund its activities. This transparency fosters confidence and facilitates informed connections with all parties.

The cash flow statement is crucial for informed decision-making, providing insights into cash inflows and outflows to guide investments, funding, and daily operations. It also aids in business planning, helping companies manage cash and plan for future financial needs to ensure long-term growth. Accounting management software like ScaleOcean further streamlines this process by automating financial statement preparation, ensuring accuracy and timely insights for better financial decisions.

FAQ:

1. What is the cash flow statement?

A cash flow statement is a financial report that tracks the movement of cash into and out of a business over a defined period. It offers a clear picture of a company’s cash management, highlighting its ability to meet short-term liabilities and maintain ongoing operations.

2. What are the three types of cash flow statements?

The three key types of cash flow statements are:

1. Operating Activities: Cash flows that result from the company’s regular business operations, such as sales revenue and payments to suppliers or staff.

2. Investing Activities: Cash flows associated with the acquisition and disposal of long-term assets like property, equipment, or investments.

3. Financing Activities: Cash flows linked to the company’s capital, including borrowing, repaying loans, issuing shares, or paying dividends.

3. How do I calculate a cash flow statement?

To prepare a cash flow statement, begin with the net income shown on the income statement. Adjust for non-cash items like depreciation and changes in working capital, such as changes in receivables and payables. Then, determine cash flows from operating, investing, and financing activities, ensuring to account for both inflows and outflows in each section.

4. What is the purpose of the statement of cash flows?

The statement of cash flows serves to provide a comprehensive view of how cash is generated and used by a business. It is essential for evaluating a company’s liquidity, operational performance, and its capacity to fund future growth or meet financial obligations, offering valuable insights for both management and investors.