Poor capital budgeting can leave a business stuck with projects that drain cash and miss the mark. Without a solid plan, companies risk making expensive mistakes that waste resources and eventually threaten their long-term growth.

According to the World Bank Group, Singapore’s GDP has averaged 7% since independence, with over 9% in its first 25 years. This fast-paced success shows why smart capital allocation is so vital for any business trying to stay ahead in a high-stakes economic market.

This article explores the fundamentals and best practices of capital budgeting, including key techniques, evaluation methods, and risk management strategies. It covers how businesses can prioritize projects, assess financial viability, and monitor performance to make data-driven decisions.

By reading through the discussion, business leaders will gain practical insights into structuring capital budgets, using accounting tools effectively, and ensuring that investment choices align with long-term growth objectives.

- Capital budgeting is the process businesses use to evaluate, prioritize, and select long-term, high-cost investments or potential major projects.

- Capital budgeting methods like NPV, IRR, and Payback Period help businesses evaluate investment opportunities by considering cash flows, risks, and returns.

- Best practices for capital budgeting, like prioritizing cash flows and using conservative estimates, help businesses make informed, strategic investment decisions.

- ScaleOcean accounting software simplifies capital budgeting by automating processes, integrating real-time data, and improving transparency, helping businesses achieve higher ROI and more accurate financial planning.

What is Capital Budgeting?

Capital budgeting is the process businesses use to evaluate, prioritize, and select long-term, high-cost investments or potential major projects. It involves planning and managing enormous budgets, ensuring that they allocate funds efficiently to initiatives that will yield the maximum results.

This strategy helps businesses identify investments that align with long-term goals and generate value over time. It is a crucial process for various industries, including technology and manufacturing, where large-scale investment decisions are needed.

From purchasing new equipment to expanding facilities or entering new markets, capital budgeting ensures that the right projects are selected. This process is key to achieving long-term success and maximizing return on investment.

Why Capital Budgeting Matters?

Capital budgeting allows organizations to make informed investment choices, especially when resources are limited. It ensures cash is directed toward high-return projects, promoting growth and financial stability by optimizing every dollar spent.

Good capital budgeting helps businesses maintain a competitive advantage by aligning investments with strategic goals. It’s essential for planning, ensuring effective resource allocation, and supporting long-term growth, securing the company’s future financial health.

Understanding opportunity cost is key to allocating resources to projects with the highest potential benefits, ensuring long-term growth. This approach is vital for determining a company’s future financial health and sustaining its growth.

How Capital Budgeting Works?

Capital budgeting is the structured process used by companies to evaluate and authorize significant spending on long-term projects. It serves as a financial filter to ensure only the most viable investments move forward.

To turn complex financial data into actionable results, businesses typically follow this systematic operational flow:

1. Practical Application in Business

Capital budgeting is an essential process in everyday business decisions, helping companies figure out where to invest their resources. By carefully analyzing potential projects, businesses can ensure they’re focusing on the ones that will bring in the best returns.

In real-life situations, companies follow a structured process to assess each investment opportunity. This helps them prioritize projects, allocate resources efficiently, and make sure their investments support their overall business goals.

2. Estimating Expenses, Earnings, and Potential Risks

To make informed decisions, businesses must accurately estimate costs, expected earnings, and potential risks. This ensures they’re financially prepared for challenges, so they don’t face surprises. The cost control process helps keep spending in check and resources optimized.

Using financial models and data analysis, companies predict expenses and revenues. By factoring in potential risks, they can confidently make investment decisions that safeguard their resources and deliver long-term value.

3. Importance of Discounting and Cash Flow Evaluation

When making investment decisions, discounting future cash flows is key. This helps businesses determine if future returns justify the initial investment, ensuring that they make sound choices that will benefit them in the long term. The standard costing method can also help set financial benchmarks.

Cash flow analysis gives businesses a snapshot of an investment’s financial health. By comparing the cash coming in with what’s going out, they can confirm whether the project will meet expectations and generate the returns they need over time.

4. Making Decisions Based on Profitability and Strategy

Capital budgeting decisions hinge on both profitability and strategic fit. It’s about choosing investments that not only offer great returns but also align with the company’s long-term goals and future direction.

Businesses evaluate each project’s potential return and how it fits with their broader strategy. This ensures investments contribute to financial growth and also help the company strengthen its position in the market for future success.

Key Objectives of Capital Budgeting

Capital budgeting serves as a strategic roadmap for a company’s financial future. It ensures that every dollar spent on major projects aligns with long-term goals while maximizing overall shareholder value.

To achieve sustainable growth, businesses must focus on these primary financial and strategic targets:

1. Choosing High-Return Projects

The main goal of capital budgeting is to focus on projects that bring in the highest returns. Businesses need to carefully weigh potential profits against costs to ensure they’re putting money into projects that truly drive growth.

This approach helps companies avoid wasting resources on projects that don’t add much value. By picking the right projects, businesses can make sure they’re investing wisely, which ultimately leads to sustainable success and growth over time.

2. Managing Capital Outlays

Managing capital expenditures is key to keeping spending in check while maximizing returns. By tracking costs carefully, companies can prevent overspending and ensure their funds are directed towards projects that really make a difference.

Capital budgeting sets the stage for clear guidelines on how money is spent. By ensuring that resources go to high-return projects, businesses can optimize their budget and avoid unnecessary costs, which helps maintain long-term profitability.

3. Identifying Optimal Funding Sources

Capital budgeting also helps businesses figure out the best way to fund their projects, whether it’s through loans, equity, or internal cash flow. Picking the right funding source makes it easier to control costs and ensures the company is financially stable.

Understanding the right way to finance each project is crucial. By choosing funding methods with the best balance of cost and risk, businesses can make sure they’re getting the most value from their investments, without overburdening their finances.

4. Reducing Risk

One of the key aspects of capital budgeting is minimizing risks. Companies need to assess the potential risks of each project so they avoid taking on investments that could lead to financial instability.

With the right tools, like risk analysis and sensitivity testing, capital budgeting helps businesses make informed decisions. This ensures that only projects with manageable risks are selected, protecting the company’s financial future and keeping things on track.

5. Achieving Strategic Fit

Capital budgeting helps businesses make sure their investments are in line with their long-term goals. It’s not just about picking the highest-return projects but also ensuring they fit the company’s strategy and overall mission.

When companies focus on projects that support their core values and objectives, they create more cohesion in their operations. This makes sure every project contributes to the bigger picture, which is crucial for maintaining growth and success in the long run.

Main Features of Capital Budgeting

Capital budgeting is defined by its long-term impact and the substantial financial commitments it requires. These core features help businesses navigate the complexities of large-scale investment and risk management.

To understand how these investments shape a company’s future, consider these essential defining characteristics:

1. Emphasis on Long-Term Goals

Capital budgeting is all about looking at the long game. It ensures that investments align with a company’s future vision, helping to plan for sustainable growth rather than just quick wins. Focusing on long-term benefits supports lasting success.

By prioritizing future value, capital budgeting helps businesses make decisions that will continue to pay off in the long run. This approach ensures that resources are used effectively to maintain competitiveness and drive growth over time.

2. Significant Capital Investment

Capital budgeting often involves making large financial commitments, which makes it a key part of business planning. These significant investments impact cash flow, so it’s crucial to assess whether the return is worth the cost.

With large amounts of capital at stake, businesses need to carefully evaluate each project. This ensures that funds are allocated wisely, contributing to profitability and making the most out of every investment made.

3. Involves Risk and Uncertainty

Every investment carries some level of risk, and capital budgeting helps businesses understand and manage that uncertainty. It allows companies to make informed choices, giving them the tools to assess whether the rewards outweigh the risks.

By recognizing and preparing for potential challenges, capital budgeting helps businesses minimize the chances of failure. The ability to weigh risks allows companies to make better decisions that align with their goals and risk tolerance.

4. Irreversible Investment Choices

In capital budgeting, decisions are often hard to reverse. Once a company invests its resources, it can’t take them back, so it’s important to evaluate the long-term impact thoroughly.

These irreversible choices make it critical to plan and think carefully about each investment. With proper planning, capital budgeting helps minimize the risk of making decisions that could hurt the company down the road.

5. Focus on Cash Flow Management

Cash flow is at the heart of capital budgeting. Managing both incoming and outgoing cash is key to making sure investments are worthwhile and can support the business in the long term.

By paying attention to cash flow, businesses can ensure their investments will provide the returns they need. Proper cash flow management allows companies to adjust their plans as needed, keeping the project financially viable over time.

6. Strategic Significance

Capital budgeting isn’t just about money when it’s also about aligning investments with the company’s long-term strategy. It helps businesses focus on projects that support their vision, ensuring that each investment contributes to growth and competitive advantage.

By making sure investments align with strategic objectives, businesses avoid wasting resources on projects that don’t fit the bigger picture. This approach ensures that every decision drives the company closer to its goals and helps maintain its position in the market.

7. Includes Key Financial Principles

Capital budgeting is grounded in solid financial principles, like the time value of money and risk assessment. According to the Monetary Authority of Singapore, the Register is a public record of individuals conducting regulated financial activities under the SFA.

These financial principles guide companies in making smart decisions that maximize returns. Capital budgeting ensures businesses stay focused on projects that offer the best growth potential, all while keeping financial health in check.

8. Assists in Investment Prioritization

Capital budgeting is essential when it comes to prioritizing where to put your money. By evaluating each project’s return and risk, businesses can focus on the ones that offer the highest growth potential.

This prioritization helps businesses make the best use of their resources. Capital budgeting helps decision-makers balance competing demands, ensuring investments align with strategic goals and contribute to overall success.

Factors Affecting Capital Budgeting

A variety of factors influence capital budgeting decisions, determining how a corporation invests its resources. Understanding these aspects leads to improved financial planning and more educated investing decisions. Capital budgeting decisions are heavily influenced by a number of factors, including capital structure, the economic environment, and management priorities.

- Investment Size: The total capital required impacts liquidity and risk. Larger projects demand deeper scrutiny to ensure they don’t strain the company’s financial health.

- Projected Returns: Expected cash flows determine if a project is profitable. This is the primary driver for choosing investments that add the most long-term value.

- Risk and Uncertainty: Potential market shifts or failures carry dangers. Assessing these risks prevents a company from overextending into projects with unstable outcomes.

- Capital Costs: The cost of borrowing or using equity affects feasibility. Returns must exceed the cost of capital for any project to remain financially viable. Prepaid expenses examples, like insurance or rent, are also considered to ensure accurate financial forecasting.

- Strategic Alignment: Projects must fit the company’s long-term vision. Even profitable ventures are rejected if they do not support the brand’s primary goals.

- Regulatory Factors: Legal requirements and tax policies change profitability. Staying compliant is essential to avoid fines and major operational disruptions.

- Market Dynamics: Shifts in consumer demand and competitor actions influence success. Understanding trends helps time investments to capture the highest growth.

- Technological Advancements: Rapid innovation can make current projects obsolete. Budgeting must account for tech shifts to ensure investments remain competitive.

- Social and Environmental Considerations: Modern firms must weigh their impact on society. ESG factors play a huge role in maintaining reputation and securing ethical funding.

- Internal Influences: Company culture and management expertise shape budget choices. These factors determine how resources are distributed and which areas get priority.

Capital Budgeting Processes

The capital budgeting process is a systematic series of steps used to evaluate the long-term economic worth of an investment. It transforms raw financial data into a structured plan for sustainable corporate growth.

To ensure every project contributes to the company’s success, firms follow this rigorous operational workflow:

1. Recognizing Investment Opportunities

The first step in capital budgeting is identifying potential investment opportunities. This involves scanning the market for projects that could align with the company’s goals and present opportunities for growth and expansion.

By spotting promising ventures early, businesses can allocate resources to projects that are most likely to provide long-term value. It’s crucial to ensure that these opportunities align with the company’s overall strategy and objectives.

2. Assessing Viability & Cash Flow Projections

Once investment opportunities are identified, evaluating their feasibility becomes key. This step involves analyzing how much capital is needed and projecting future cash flows to determine whether the investment will be financially viable.

Cash flow projections help estimate the potential returns from an investment and identify any risks that may affect profitability. A thorough assessment ensures that businesses are making informed decisions backed by realistic financial forecasts.

3. Estimating Costs and Potential Returns

The next step in capital budgeting is estimating the costs involved and the potential returns of each investment. This includes both initial costs and ongoing expenses required for the project, along with expected revenue over time.

By carefully estimating these figures using an expense report, businesses can better assess the profitability of each investment option. This step is essential for ensuring that investments will provide a healthy return compared to the costs incurred.

4. Using Capital Budgeting Techniques

Capital budgeting methods, such as Net Present Value (NPV) or Internal Rate of Return (IRR), are applied to evaluate the financial viability of each investment. These techniques help businesses compare projects and select the best ones based on their financial metrics.

These methods provide a systematic approach to investment analysis, helping companies make well-informed decisions. They ensure that resources are allocated effectively to maximize returns while minimizing risk.

5. Selecting the Optimal Investment Choice

After applying various capital budgeting methods, businesses must select the investment that best aligns with their financial and strategic goals. This choice involves considering not only the financial projections but also the risks and long-term benefits.

Choosing the best option ensures that the company invests in projects with the highest potential for success. It involves balancing risk and reward while ensuring the project contributes to the company’s growth and future objectives.

6. Executing and Tracking the Investment

After making the final investment decision, implementation begins. This involves setting up the project and closely monitoring its progress to ensure it stays on track and meets the expected financial and strategic goals.

Ongoing monitoring helps identify any issues or deviations from the plan early on. By staying on top of the project’s progress, businesses can adjust strategies as needed to maximize returns and ensure successful outcomes.

Capital Budgeting Methods and Metrics

Capital budgeting strategies and indicators are critical for assessing investment opportunities and making sound financial decisions. These strategies assist in determining if a project will provide good returns and fit the company’s strategic objectives.

The methodologies range from simple to more complex approaches, providing many ways to assess a project’s financial viability. Here are the capital budgeting Methods and metrics:

1. Payback Period

The payback period measures the time it takes to recover an investment. It’s a simple method widely used by companies focused on liquidity, allowing them to quickly assess how soon an investment will pay back its initial costs. Here is the formula to calculate the payback period:

Payback Period = Initial Investment ÷ Annual Cash Inflow

However, the payback period doesn’t consider the time value of money or cash flows beyond the payback point. This limits its accuracy, especially for long-term projects where future benefits are not factored into the evaluation.

2. Discounted Payback Period

This method builds on the payback period by accounting for the time value of money. It discounts future cash inflows to reflect their present value, offering a more accurate picture of the time needed to recover an investment. Here is the formula to calculate the discounted payback period:

Discounted Payback Period = Time when Σ (Cash Inflow_t ÷ (1+r)^t) = Initial Investment

By considering the time value of money, it improves the accuracy of liquidity assessments. This method is especially useful for long-term projects with cash flows that vary over time, ensuring later inflows are appropriately valued.

3. Net Present Value (NPV)

NPV calculates the present value of expected cash inflows and outflows, considering the time value of money. A positive NPV means the project is expected to generate value above its cost, while a negative NPV suggests it should be rejected. Here is the formula for calculating NPV:

NPV = Σ (Cash Inflow_t ÷ (1+r)^t) − Initial Investment

NPV helps businesses compare different projects consistently, making it a key method for evaluating investment opportunities. It’s widely used because it provides a clear indication of whether a project will add value to the company over its lifespan.

4. Internal Rate of Return (IRR)

IRR is the discount rate that makes a project’s NPV equal to zero. It represents the expected return of a project and helps compare investments with the company’s required rate of return. Projects with an IRR higher than the required rate are considered favorable. Here is the formula to calculate IRR:

0 = Σ (Cash Inflow_t ÷ (1+IRR)^t) − Initial Investment

IRR is particularly useful when multiple projects compete for the same funds, helping businesses rank investment options. However, it can produce multiple values for projects with unconventional cash flows, making it less reliable in such cases.

5. Modified Internal Rate of Return (MIRR)

MIRR improves upon IRR by considering reinvestment at a realistic rate, instead of assuming cash flows are reinvested at the IRR. This provides a more accurate picture of a project’s profitability, especially for long-term investments with fluctuating inflows.

MIRR = (Terminal Value of Cash Inflows ÷ Present Value of Cash Outflows)^(1/n) − 1

By offering a more realistic estimate of returns, MIRR helps businesses make better investment decisions. It’s particularly useful for projects with irregular cash flows or those spanning long durations, giving managers a clearer view of potential outcomes.

6. Profitability Index (PI)

PI measures the ratio of the present value of future cash flows to the initial investment. A PI greater than 1 indicates a financially viable project. This method is useful for ranking projects when capital is limited, ensuring resources are allocated efficiently. Here is the formula for calculating PI:

PI = Present Value of Future Cash Flows ÷ Initial Investment

By considering the time value of money, PI provides a more accurate evaluation compared to methods like the payback period. It helps businesses prioritize investments, ensuring that scarce resources are directed to projects with the best potential returns.

7. Discounted Cash Flow (DCF) Analysis

DCF calculates the present value of all expected cash inflows and outflows, taking into account the time value of money. This method helps businesses compare projects of different sizes, durations, and risks. It is foundational for NPV and other budgeting methods. Here is the formula for DCF:

DCF = Σ (Cash Inflow_t ÷ (1+r)^t) − Σ (Cash Outflow_t ÷ (1+r)^t)

DCF is essential for long-term financial planning and investment decisions. Accurate cash flow forecasts and discount rates are crucial for reliable results, as any inaccuracies can affect the outcome and lead to poor decision-making.

8. Equivalent Annuity Method

The equivalent annuity method converts NPV into equal annual cash flows, allowing businesses to compare projects with varying lifespans. This method is ideal for mutually exclusive projects or when evaluating options with unequal durations. Here is the formula for calculating EAA:

EAA = (NPV × r) ÷ (1 − (1+r)^−n)

By annualizing the value of each project, it provides a fair comparison for businesses to make informed decisions. This method is particularly useful when companies need to choose between investments of different lengths or those with different cash flow patterns.

9. Throughput Analysis

Throughput analysis evaluates projects based on their ability to increase system-wide output, rather than focusing solely on cost savings. This is especially relevant in manufacturing, where projects that improve overall flow are prioritized.

For example, a factory line bottleneck can be resolved by investing in faster machinery, which results in overall throughput increases, boosting profitability more than investing in unconstrained areas.

By focusing on bottlenecks and system efficiencies, throughput analysis ensures that capital is invested in areas that maximize overall operational performance. This approach boosts profitability more than investments in areas that are already functioning optimally.

10. Constraint Analysis

Constraint analysis identifies operational or market limitations and prioritizes projects that alleviate these bottlenecks. This method ensures that capital is allocated efficiently to projects that improve performance and address the most critical resource constraints.

For example, constraint analysis would prioritize expanding dining space rather than adding more kitchen equipment. By focusing on the true constraints, businesses can make better use of their available resources and drive growth.

11. Cost Avoidance Analysis

Cost avoidance analysis evaluates projects that prevent future expenses or inefficiencies. By prioritizing projects that eliminate costly problems, businesses can save money in the long run. It considers opportunity costs and is valuable for long-term financial planning.

For example, investing in automated accounting software prevents the need for additional bookkeepers, equals to savings that are considered a return on investment.

This type of analysis ensures that resources are used to eliminate avoidable costs and enhance financial sustainability. It helps businesses focus on long-term savings by preventing future expenses before they occur.

12. Real Options Analysis

Real options analysis provides flexibility by evaluating a project’s ability to adapt to future changes. It considers the possibility of delaying, expanding, or exiting a project depending on market conditions, which is crucial for uncertain ventures.

Effective expense management strategies also play a key role in these decisions. For instance, a tech company invests in a facility, but can delay expansion if market conditions are unfavorable, which is where flexibility adds value beyond NPV.

By adding flexibility to the NPV method, real options analysis helps businesses account for changes that may affect cash flows. This approach is particularly useful in dynamic industries where future decisions can significantly impact the project’s value.

Major Challenges in Capital Budgeting

Capital budgeting is not without obstacles. Despite its importance, organizations frequently confront numerous challenges when making long-term investment decisions. These problems can have an impact on the accuracy and reliability of capital budgeting, as well as the overall success of projects. The challenges are as follows:

1. Inaccurate Cash Flow Projections

Capital budgeting relies on estimating future cash flows, but these projections can sometimes miss the mark. If cash flows are overestimated or underestimated, it can lead to poor investment decisions that hurt the company’s financial health.

When cash flow projections are inaccurate, it becomes hard to determine the true value of a project. This makes it crucial for businesses to carefully evaluate future inflows and outflows to avoid making decisions based on faulty assumptions.

2. Uncertainty in Return Timing

One of the challenges in capital budgeting is the uncertainty about when returns will actually materialize. Many projects take time to generate cash flows, and delays or unforeseen problems can affect when those returns are realized.

Changes in market conditions, supply chain disruptions, or unforeseen obstacles can all delay expected returns. It’s important to plan for these delays and factor them into the capital budgeting process to avoid unpleasant surprises later on.

3. Difficulty in Selecting the Appropriate Discount Rate

Choosing the right discount rate is essential but can be difficult. An incorrect rate can significantly impact a project’s evaluation, either overstating or understating its value. Getting this wrong can lead to misguided investment decisions.

The discount rate should reflect the company’s cost of capital and risk level. If it’s set too high or too low, it can result in a distorted view of the project’s potential, making it harder to assess whether the investment is worthwhile.

4. Reliance on Estimates and Assumptions

Capital budgeting is often based on estimates and assumptions, which can be uncertain. These projections about future cash flows, costs, and risks are not always accurate, which can lead to flawed investment decisions.

Since estimates rely on limited information and assumptions, businesses should be aware that things might not go as planned. Constant adjustments are necessary to ensure that the investment analysis remains relevant as conditions evolve.

5. Time-Consuming and Complex Process

The process of capital budgeting can be long and complex, involving lots of data analysis and careful planning. For businesses, this can be time-consuming, as they need to evaluate numerous factors before making a decision.

Despite its complexity, capital budgeting is essential for ensuring that investments are made wisely. While the process can take time, it’s a necessary step for companies to ensure they’re making the right decisions for their future.

6. Limited Ability to Factor in Qualitative Aspects

Capital budgeting typically focuses on quantitative factors like cash flows and financial returns. However, this can leave out important qualitative aspects, such as employee satisfaction or brand reputation, which can also impact the success of a project.

While numbers are critical, it’s important not to overlook non-financial factors that play a role in the long-term success of a project. Taking into account the qualitative benefits can provide a more holistic view of the investment’s true value.

7. Exposure to Risk and Uncertainty

Every investment carries some risk, and capital budgeting does not eliminate this uncertainty. Market fluctuations, technological changes, or unforeseen challenges can impact the expected returns and overall project success.

Being aware of these risks allows businesses to take a more cautious approach and make better-informed decisions. It’s vital to understand the potential downsides of a project and be ready to adjust the plan if things don’t go as expected.

8. Constraints Due to Capital Rationing

Capital rationing happens when a business has limited resources and has to choose between different investment opportunities. This can prevent a company from pursuing all the projects it wants, potentially causing it to miss out on valuable opportunities.

When capital is constrained, businesses must prioritize projects that offer the highest return. This can lead to tough decisions, but effective capital rationing ensures that the company is using its resources in the most impactful way possible.

9. Regulatory and Tax Implications

Capital budgeting needs to consider regulatory and tax factors, as changes in laws or tax policies can affect the financial viability of a project. These factors can alter the expected costs and returns, making them essential to account for in the planning process.

Ignoring regulatory changes may lead to increased business expenses that were not anticipated, impacting project profitability. Staying informed about tax and legal changes ensures that businesses can plan effectively and avoid unexpected financial burdens.

10. Challenges with Data and Integration

For capital budgeting to be effective, businesses need accurate and integrated data from various departments. However, gathering and consolidating this information can be challenging, and poor data integration can lead to mistakes in decision-making.

Having the right systems in place to collect, manage, and analyze data is essential for ensuring that capital budgeting decisions are based on reliable and consistent information. Without proper data integration, it’s hard to make well-informed investment choices.

11. Misalignment with Strategic Goals

While capital budgeting focuses on financial returns, it’s not always aligned with a company’s long-term strategy. Some projects may offer high returns but don’t align with the company’s core objectives or vision, leading to misallocation of resources.

Capital budgeting decisions must support the company’s overall mission and strategy. By ensuring that investments align with strategic goals, businesses can avoid pursuing projects that may not contribute to their long-term success.

Key Report Types & Their Use Cases

Key reports in capital budgeting are critical for monitoring, managing, and assessing investment decisions. They assist firms in keeping stakeholders informed and projects on schedule. These reports also include information about financial performance, risks, and strategic alignment. The following are some of the important report kinds and their use cases:

1. Capital Expenditure (CAPEX) Proposal Reports

Capital expenditure reports are generated before project approval to determine the feasibility of an investment. They often include a project summary that explains the project’s goal, scope, and strategic alignment.

Financial criteria such as NPV and IRR, risk assessments, an implementation timeframe, and a cost-benefit analysis are all included to ensure that the project is financially viable and in line with the company’s goals.

2. Project Monitoring & Progress Reports

During project execution, these reports give regular updates on the project’s status. They display the percentage of completion, budget spent, cash flow status, and any variations.

These reports are critical for keeping stakeholders informed about the project’s progress and identifying deviations from the original plan, allowing adjustments to be made in real time.

3. Periodic Capital Expenditure Review Reports

These reports are usually published weekly or annually to evaluate long-term investment performance. They compare the actual capital expenditures report to planned budgets to determine whether projects are reaching financial and strategic objectives.

These assessments assist firms in ensuring that capital investments are providing the intended returns and remain consistent with the overall business strategy.

4. Capital Budget Presentations

Capital budget presentations provide a visual depiction of funding sources, asset categories, and project objectives. They employ infographics and charts to display complex financial data in an understandable style, allowing executives or boards to make better decisions about future investments.

Best Practices For Capital Budgeting

Capital budgeting is an important practice for businesses to make the best use of resources and achieve long-term success. Businesses can make better investment decisions by adhering to best practices and strategic insights.

Here are essential recommendations for improving your capital budgeting process:

1. Prioritize Cash Flows Over Net Income

When assessing investments, it’s crucial to focus on cash flows rather than net income. Cash flows represent the real money the business will generate, making them a more reliable gauge of a project’s financial viability.

Net income includes non-cash elements like depreciation that don’t actually affect cash. By focusing on cash flows, businesses can make more informed investment decisions based on actual financial performance.

2. Rely on Conservative Estimates

Capital budgeting works best when it’s based on conservative estimates. By being cautious with projections, businesses can avoid overestimating returns, which helps reduce the risk of underperforming investments.

Conservative estimates help businesses plan for uncertainties. This approach provides a cushion for unexpected changes, ensuring that projects remain financially feasible even if conditions change.

3. Accurately Forecast the Timing of Cash Flows

Timing is everything when it comes to capital budgeting. Correctly predicting when cash inflows and outflows will occur allows businesses to better assess a project’s true value over time.

If cash flow timing is inaccurate, it can lead to miscalculations, skewing the project’s financial picture. Properly forecasting when money will come in and go out provides a clearer and more reliable view of the project’s impact.

4. Exclude Non-Cash and Financing Costs

Capital budgeting should focus on real cash flows, leaving out non-cash items like depreciation or financing costs. These factors don’t affect the actual cash flow and can give a false impression of a project’s financial viability.

By concentrating on tangible cash inflows and outflows, businesses can make more accurate evaluations. This keeps the capital budgeting process grounded in what truly impacts a project’s bottom line.

5. Build a Robust Procedural Framework

A solid procedural framework for capital budgeting ensures consistency in decision-making. With a structured process in place, businesses can evaluate investments systematically, reducing the risk of errors or oversights.

This framework should include all key steps, like cash flow analysis and risk assessments. By sticking to this structure, businesses make more reliable decisions and boost their chances of selecting successful projects.

6. Incorporate Reviews and Feedback Mechanisms

Capital budgeting shouldn’t be a one-off task. Regular reviews and feedback are essential to stay on track and adjust projections if needed. This allows businesses to catch potential issues early and course-correct before it’s too late.

Getting input from various stakeholders ensures better decision-making. These feedback loops refine strategies, highlight any challenges, and help keep projects aligned with the company’s broader goals.

7. Utilize Scenario and Sensitivity Analysis

Scenario and sensitivity analysis are key tools in capital budgeting. These methods allow businesses to test different assumptions and see how they impact the project’s potential returns, helping to understand the associated risks.

By considering various “what-if” scenarios, businesses can prepare for market shifts or unexpected changes. This analysis gives a clearer picture of a project’s success, even if conditions evolve in unpredictable ways.

8. Ensure Alignment with Strategic Goals

Every capital budgeting decision should align with the company’s long-term strategy. When investments match the company’s vision, resources are better allocated to drive growth and stay focused on key objectives.

When projects support strategic goals, they not only generate financial returns but also reinforce the company’s mission. This ensures that every decision made adds value and contributes to the business’s overall success.

9. Leverage Technology and Integrated Systems

Technology and integrated systems can really streamline the capital budgeting process. By using automated tools for data collection and analysis, businesses can save time and make better decisions faster.

With the right tech, businesses reduce human error and ensure that all factors are considered. This allows for a smoother, more effective capital budgeting process that leads to smarter investment choices.

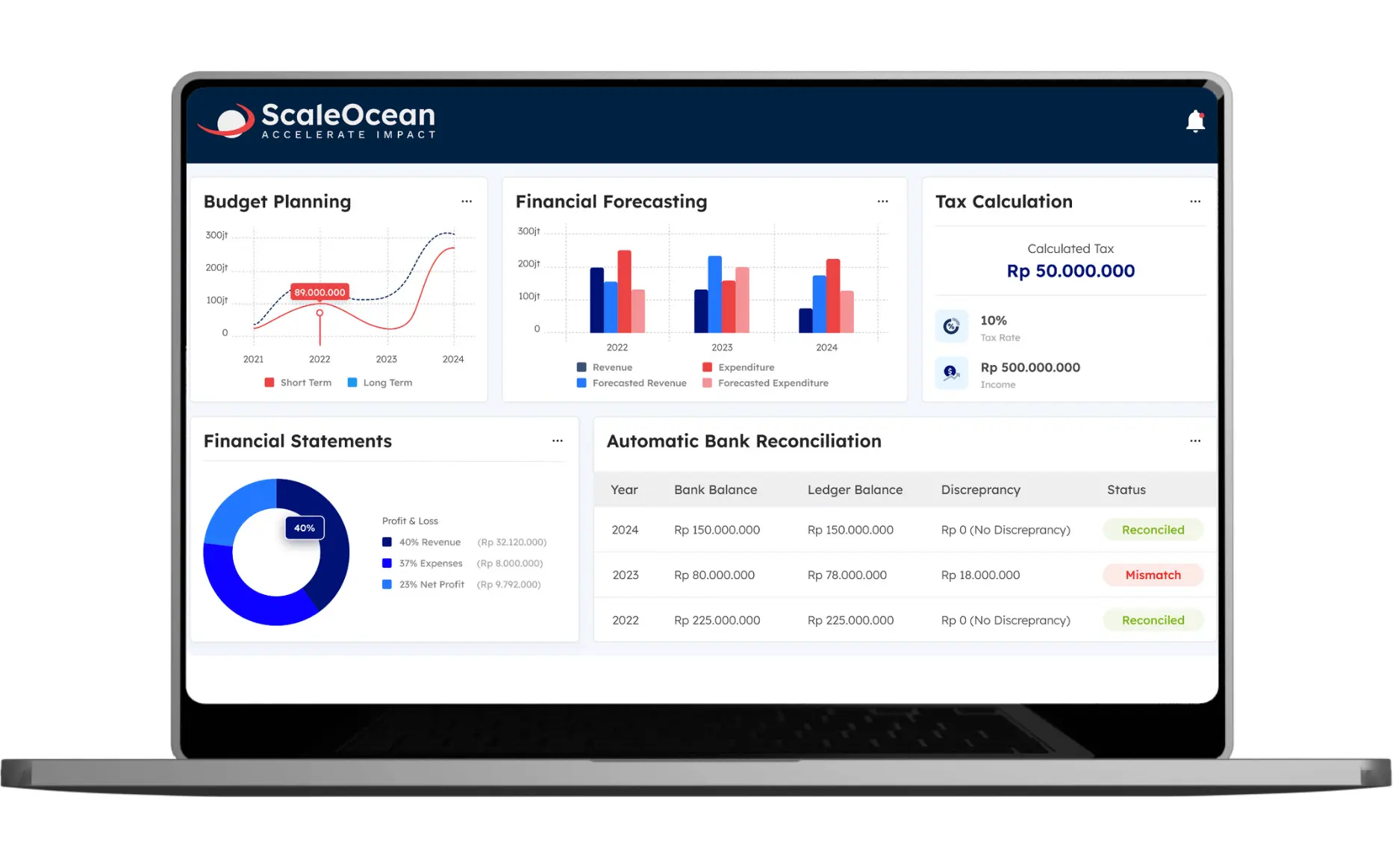

Enabling Smarter Capital Budgeting with ScaleOcean Accounting Software

Traditional spreadsheet budgeting lacks teamwork and is prone to complications. ScaleOcean’s expense software overcomes these difficulties with automation, real-time tracking, and seamless bank connectivity. It streamlines financial reporting, increases transparency, and promotes data-driven decision-making.

Traditional spreadsheet budgeting lacks teamwork and is prone to complications. ScaleOcean’s expense software overcomes these difficulties with automation, real-time tracking, and seamless bank connectivity. It streamlines financial reporting, increases transparency, and promotes data-driven decision-making.

ScaleOcean improves financial control and post-implementation performance, resulting in higher ROI and more accurate capital budgeting outcomes. ScaleOcean is a strong solution for streamlining capital budgeting, allowing firms to make strategic and informed decisions.

With a free demo, businesses can see how the program helps improve budgeting and financial planning. Additionally, ScaleOcean is qualified for the CTC grant, which will help enterprises improve their capital management. Below is a list of key features of the ScaleOcean software:

- Integrated Financial Platform for Accurate Budgeting: ScaleOcean integrates project-level budgeting, forecasting, and cash flow analysis for accurate, strategic financial decisions.

- Real Time Collaboration & Customizable Reporting: The cloud-based solution enables real-time teamwork and customizable reports tailored to capital budgeting needs.

- Multi-Level Financial Analysis for Capital Decisions: Advanced financial tools offer in-depth analysis for informed and strategic capital project decisions.

- Automated Reconciliation & Unlimited User Access: Automates financial reconciliation and offers unlimited user access at a fixed price, ideal for growing businesses.

- Cloud-Based Flexibility & Enhanced Financial Control: Provides flexible, real-time financial management, improving capital budget control and optimizing ROI.

Conclusion

Capital budgeting is vital for making sound, strategic investment decisions. It enables businesses to deploy capital more efficiently, directing resources toward projects that promote long-term growth. A structured approach to budgeting helps firms prioritize investments and optimize financial results.

Businesses that use sound procedures and risk-aware practices can balance profitability with long-term resilience. ScaleOcean’s expense system improves upon this by offering real-time tracking, automatic reporting, and data-driven insights. This ensures optimal budgeting and promotes both immediate and long-term success.

FAQ:

1. Why is it called capital budgeting?

It’s called capital budgeting because it focuses on large-scale capital projects rather than everyday operational costs. The process involves creating a budget for these investments and evaluating whether their future benefits justify the current cost and risks.

2. What is another name for capital budgeting?

Capital budgeting is also referred to as investment appraisal. This term highlights the process of assessing and evaluating potential investments to determine their financial viability and long-term returns.

3. What is an example of capital budgeting?

A typical example of capital budgeting is a company evaluating whether to expand its operations by building a new facility. This involves calculating the upfront construction costs, expected revenue increase, and long-term operational savings, and using methods such as NPV or IRR to determine whether the investment is worth pursuing.

4. Who is responsible for capital budgeting?

The Chief Financial Officer (CFO) plays a key role in overseeing the financial stability of a company. Their duties include managing cash flow, planning mergers or acquisitions, conducting capital analysis, and handling capital budgeting decisions.