Bank reconciliation is a crucial financial procedure that involves comparing the company’s financial records with the bank statement to ensure consistency. This method is particularly important for Singapore businesses, where meeting compliance regulations and financial transparency is a must.

A precise reconciliation can help companies monitor cash flows, identify discrepancies, and minimise errors that could impact their financial records. Maintaining accurate accounting is one of the most crucial things to do to stay one step ahead.

Keeping a regular bank reconciliation will not only ensure adherence to local rules, but it will also provide valuable data regarding tash management. The automation of this process is also becoming increasingly vital for businesses to remain efficient and competitive, in order to minimise human mistakes, save time, and make quicker yet well-informed decisions.

- Bank reconciliation is the process of comparing a company’s financial records to the bank’s records to ensure consistency, preventing errors like missed deposits and mishandled payments.

- The steps for doing bank reconciliation include gathering necessary documents, comparing records, identifying discrepancies, making adjustments, and finalizing the reconciliation to ensure accurate financial reporting.

- The bank reconciliation template helps organizations match internal records with the bank’s statement, ensuring accuracy, reducing errors, and supporting better decision-making.

- ScaleOcean ERP software automates the bank reconciliation process by integrating financial data with bank statements, improving accuracy, efficiency, and timeliness while reducing manual errors.

What Is Bank Reconciliation?

The process of comparing the financial records of a business with the bank’s records to ensure that the records are consistent is called bank reconciliation. This practice is essential for businesses to maintain up-to-date financial records because it ensures that all transactions are documented in the business’s accounts and appear in the bank statement.

Reconciliation reduces differences, including mismanaged payments, missed deposits, etc., which may result in a difference in the financial information being reported. Bank reconciliation is essential in company financing documents management for keeping company funds aligned with the bank’s records, ensuring the accuracy of company accounting documents.

The act of reconciling regularly enables companies to readily discover errors, achieve better monetary reporting, and manage cash flow more efficiently, as it helps to increase financial transparency and avoid misstatements that may impact decision-making. Smooth and timely reconciliation depends on the size of the firm and on transaction volume. The following are the main points of when to execute bank reconciliation:

1. Daily

Most companies handling big payments benefit when reconciling accounts every day. A shop or online seller finds that this rhythm fits well. Errors show up quickly, sometimes catching dishonest actions before they grow. Records stay accurate because mismatches get fixed each morning.

Over time, fewer gaps appear between expected and actual numbers. Control strengthens around money moving in and out. Budgets respond better to shifts in income or spending patterns. Fast websites support immediate views into performance data. Adjustments happen swiftly since insights arrive without delay.

2. Weekly

Most mid-level firms handle enough activity to make weekly checks practical. Instead of daily scrutiny, spacing it out helps maintain clarity without excess effort. Catching irregularities sooner tends to happen when updates occur every seven days. This rhythm supports clean records, yet avoids constant interruptions.

Small mistakes are less likely to pile up under such a routine. Precision stays high, though not at the cost of endless hours. The approach fits those wanting steady oversight minus the burden.

3. Monthly

Monthly reconciliation is excellent for small organizations with few transactions. It is an effective method for keeping accurate financial records while managing limited resources. Monthly checks allow firms to keep track of their cash flow and identify any problems that may arise without frequent oversight.

Monthly reconciliation suits small organisations handling a few transactions each month, making it ideal for accurate record-keeping when budgets are tight. Cash flow becomes easier to follow through routine reviews every thirty days, as efficiency grows when teams balance deadlines alongside fiscal oversight. This strategy enables firms to better manage their time while maintaining financial transparency and the financial control process.

The Purpose of Bank Reconciliation

Most often, bank reconciliation checks whether a company’s recorded balances align with what appears on its bank statement. Matching these details means comparing each entry – deposits, transfers out, service fees – from both sources carefully. Differences show up when timing varies, or errors slip into either set of records. What matters most is spotting those gaps quickly so corrections happen without delay.

Because every transaction gets logged properly on each side, firms avoid mismatched records. Spot checks of these entries reveal errors soon, keeping financial outcomes aligned with targets. Early detection means corrections happen before small issues grow, supporting steady financial goals.

Spotting such issues early allows a company to fix them ahead of any damage to financial records or economic stability. In the end, accuracy in reporting improves when money figures truly reflect the actual state of the business.

Why Bank Reconciliation Is Important for Businesses

Because bank reconciliation aligns a company’s books with its bank statements, it plays a key role in financial oversight. Regular matching of records helps organizations spot mistakes before they grow. Much like how absorption costing assigns expenses properly across goods made, reconciling accounts confirms each transaction appears where it should.

Accuracy improves when internal data reflects what banks report – disagreements get resolved early. Unexpectedly, small discrepancies grow into major issues when left unchecked. Because of this, matching internal records with bank statements becomes necessary for spotting errors early. Financial clarity often depends on these routine checks behind the scenes.

When figures fail to align, confusion follows – disrupting both reporting and planning. Over time, consistent verification supports trust in company data. One overlooked transaction might trigger cascading inaccuracies across departments. For that reason, regular review acts as a safeguard against unintended mistakes. Accuracy improves significantly once mismatches are identified and corrected promptly. Ultimately, staying aligned with banking partners strengthens overall business stability.

1. Keeping Financial Records Accurate

Because reconciliation happens, businesses see where money moves without guesswork. When done often, mismatches in income or spending rarely stick around, since every deposit and withdrawal gets checked against real bank activity.

Examples of financial instruments, such as loans or bonds – common types of financial tools – frequently appear in reconciliation processes, helping ensure steady and reliable reporting practices. These items support clarity across statements by aligning recorded amounts with actual obligations.

2. Preventing Fraud

Bank reconciliation is crucial to combating fraud. Discrepancies, mistakes, or unlawful transactions are rapidly identified, minimising the likelihood of fraudulent activity being undetected. Regular checks make it easier to detect any questionable activity that may otherwise result in financial loss and damage to the company’s reputation.

3. Improving Cash Flow Management

Accurate reconciliation helps businesses manage and forecast cash flow by tracking deposits, payments, and bank fees, preventing overdrafts, and aiding in future planning. According to IRAS, businesses must keep records for at least five years to ensure that income and expenses can be easily verified. This practice also supports better investment decisions and ensures compliance with tax regulations.

4. Compliance and Tax Purposes

Accurate financial records are essential for organisations to comply with regulatory and tax requirements. According to Singapore Statutes Online, bank accounts for the funds of a Town Council must be maintained, with preference given to banks incorporated in Singapore. By reconciling bank statements with internal records on a regular basis, companies ensure that their financial data is up to date and compliant with local rules and regulations. This reduces the risk of penalties and ensures that audits run smoothly.

The Formula to Calculate Bank Reconciliation

The formula for calculating bank reconciliation helps identify discrepancies between the two, allowing businesses to detect errors, omissions, or fraudulent activities. This formula ensures accurate financial reporting and helps maintain the integrity of the company’s accounting records.

Bank Statement Balance + Deposits in Transit – Outstanding Checks = Adjusted Bank Balance

5 Steps and How to Do Bank Reconciliation

Bank reconciliation is a critical activity that helps firms ensure that their financial records match the bank’s statements. Analyzing transactions and spotting inconsistencies, it provides precise cash flow management, eliminates errors, and promotes wise financial decisions.

The following are the steps to efficiently do a bank reconciliation:

1. Gather Necessary Documents

The first step in bank reconciliation is collecting all pertinent financial papers. This contains the company’s bank statement, which reveals the bank’s transaction history, as well as internal accounting records such as cash receipts, cheques issued, and any other financial papers associated with the transactions.

Having all of the relevant documents on hand ahead of time helps to streamline the process and prevents any important data from being overlooked.

2. Compare Bank and Business Records

Next, compare the company’s internal records to the bank’s statement. Carefully match each transaction indicated on the bank statement to the corresponding entries in the company’s accounting records.

Pay particular attention to any variations in transaction amounts, dates, or descriptions. This comparison will identify any discrepancies that require additional study.

3. Identify Discrepancies

Common differences that may develop during reconciliation include bank fees, deposits in transit, and unpaid checks. Other difficulties could include transactions that the bank has not yet completed or mistakes in transaction descriptions.

Identifying these differences is critical because it allows firms to pinpoint the causes and implement corrective measures.

4. Make Adjustments

Once discrepancies have been detected, make the necessary revisions to the accounting records. For example, update internal records to account for any missed bank fees or add transactions that the bank recorded but are not yet on the company’s books. If an issue cannot be fixed quickly, flag it for future study.

5. Finalize the Reconciliation

After adjusting entries and clearing up mismatches, full alignment is reached, and accuracy improves within the accounting documents once this step finishes. After finishing reconciliation, accuracy in records must be maintained, and unresolved issues must be written down and kept for later review. Every so often, an audit checks whether reconciliations stay careful.

If something does not match, it gets handled early – before touching broader financial reports. Performing a financial audit periodically can help ensure that the reconciliation process remains thorough and that any discrepancies are properly addressed before they affect the overall financial statements.

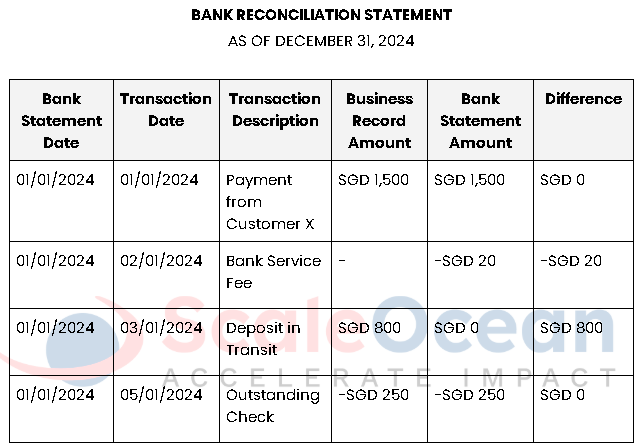

Example Template for Bank Reconciliation

This template helps organizations match each entry with their records, providing a clear overview of the reconciliation process. It enables easy identification of discrepancies between internal financial records and the bank statement.

By ensuring accuracy and efficiency, it reduces errors and fraud, supporting reliable financial management data for better decision-making and management. Below is an example of how companies can track the reconciliation process:

Challenges That Arise When Businesses Don’t Perform Bank Reconciliation

Neglecting bank reconciliation exposes firms to financial risks that might disrupt operations. Without this approach, errors might jeopardize financial integrity and result in costly blunders. If issues such as erroneous reporting and inadequate cash flow management are not addressed, they might worsen.

It is critical to recognize the hazards associated with failing to reconcile bank statements on a regular basis. The following are the primary challenges businesses may face:

1. Inaccurate Financial Reporting

Without bank reconciliation, firms risk mistakes in their financial statements, resulting in incorrect data. This can lead to poor decision-making because managers may act on inaccurate financial information.

Regular reconciliation ensures that financial reports represent the company’s true financial condition, enabling smarter business decisions. ERP for Banking industry solutions can help automate the reconciliation process, reducing the chance of errors and ensuring accurate financial reporting for banks and financial institutions.

2. Missed Opportunities for Cost Control

Neglecting regular reconciliation might lead to organizations overlooking overpayments or unneeded expenses. For example, duplicate charges or concealed costs may go unreported, reducing profitability. Businesses that reconcile their accounts regularly can identify anomalies early on, allowing for better cost control and increased savings.

3. Increased Risk of Errors and Fraud

Failure to reconcile bank statements raises the danger of unreported errors and fraud. Unrecorded transactions or fraudulent activity can go undetected, inflicting considerable financial damage. Regular reconciliation assists in identifying such difficulties, ensuring that financial records are accurate, and safeguarding the company from financial fraud.

4. Difficult Cash Flow Management

Without effective reconciliation, businesses struggle to accurately track cash flow, which can result in overdrafts or missed payments. If available finances are overstated, businesses may encounter unanticipated financial difficulties. Regular bank reconciliation provides a comprehensive picture of cash flow, allowing businesses to prevent cash shortages and better manage their finances.

Examples of Bank Reconciliation in Business

Bank reconciliation is a practical method that businesses employ to ensure that their financial records are correct and in line with their bank statements. The procedure aids in error detection, discrepancy identification, and effective cash flow management. Regular bank reconciliation can benefit a variety of firms, including small and medium-sized corporations and e-commerce companies. Here are some instances of how different organizations use bank reconciliation in their operations:

1. Small Business Example

A local retailer reconciles their bank statement regularly to reflect sales, payments, and deposits. By doing so, the store verifies that its financial records match the bank’s reported transactions. This method is critical since it identifies inconsistencies fast, such as missed payments or unreported bank fees. By addressing these issues early on, the retailer may ensure proper financial reporting and minimize possible cash flow challenges.

2. Medium Enterprise Example

A manufacturing company with worldwide transactions uses bank reconciliation to match bank payments to internal accounting records. This method facilitates foreign exchange, currency changes, and overseas payments.

Regular reconciliations help the organization prevent accounting errors and ensure correct reporting of international transactions, lowering the risk of overpayment or underreporting.

3. E-commerce Example

Bank reconciliation is critical for online businesses since it allows them to trace payments and ensure accurate order processing. By comparing payments to bank data, the company prevents missed orders and payment mistakes.

This helps to avoid shipment delays and assures smooth customer transactions, resulting in increased confidence, managing the inventory accounting process, and efficient order fulfillment.

Typical Problems Faced in Bank Reconciliation

In bank reconciliation, common problems that businesses encounter could lead to discrepancies in the financial records and bank statements. This can be for a multitude of reasons, such as unreliable financial forecasts, unusual costs, or time limits. If these discrepancies are not addressed, the financial record keeping, financial planning, and management of cash could be incorrect.

Some of the common issues that are seen in bank reconciliation below:

1. Bank Charges

Bank reconciliation is a common occurrence with unexpected bank fees. Often, the amounts paid, which may contain service charges or transaction fees, are not recognised in the company’s accounting books in time. These fees can therefore cause problems if it turns up on the bank statement but not on the company’s records. Be provided with a bank statement to review regularly and ensure the fees are reported correctly and promptly.

2. Timing Differences

Timing disparities occur when the company records transactions, such as checks issued or payments made, but the bank has not yet processed them. These delayed transactions may cause problems in the reconciliation process. To address this issue, businesses should monitor the status of all transactions and ensure that any outstanding transactions are modified when the bank processes them.

3. Human Error

Human error, such as inaccurate data entry or transaction classification, can cause disparities throughout the reconciliation process. These problems may arise when transactions are recorded manually. Businesses can reduce errors and verify that their records match the bank statement by automating the process and conducting regular assessments.

4. Uncleared Checks or Pending Transactions

Uncleared checks or pending transactions that the bank has not yet processed can cause discrepancies in the records. This happens when the firm issues payments or checks that remain unminimized, or the bank has not yet cleared them. Businesses should frequently monitor the progress of these checks and pending transactions and modify their records whenever the bank processes them.

How to Overcome Bank Reconciliation Challenges With ScaleOcean’s Accounting Software

Bank reconciliation can be difficult for organizations because of human errors, discrepancies, and time-consuming manual operations. Financial ERP software in Singapore, like ScaleOcean, automates this procedure by comparing internal financial data to bank statements, ensuring accuracy and timeliness while saving time and minimizing errors.

ScaleOcean accounting software also interacts with Bank Reconciliation Software, which streamlines and automates the entire reconciliation process, hence enhancing accuracy and efficiency.

Businesses that use real-time financial insights can make better decisions and stay on track with their budgets. ScaleOcean offers a free demo to individuals interested in exploring its features, and it is qualified for the CTC grant to help decrease installation expenses. Here are the main aspects that improve the bank reconciliation process:

- Automated Bank Reconciliation: ScaleOcean automates the reconciliation process, matching internal records with bank statements, ensuring accuracy, timeliness, and reducing manual errors.

- Real-Time Financial Insights: ScaleOcean provides up-to-date financial tracking, helping managers monitor cash flow, accounts, and transactions for quicker, informed decision-making.

- Comprehensive Integration with Other Modules: The integration of ScaleOcean’s accounting, inventory, and sales modules ensures seamless, accurate financial data across the system, reducing discrepancies.

- Efficient Error Detection and Adjustment: ScaleOcean’s ERP system quickly identifies and resolves discrepancies between bank statements and internal records, streamlining error correction.

- Time and Cost Savings through Automation: By automating transaction matching and payment processing, ScaleOcean reduces manual effort, freeing up resources for more strategic tasks.

Conclusion

Regular bank reconciliation is critical for keeping correct financial records, preventing fraud, and meeting regulatory obligations. Businesses that reconcile bank statements with internal financial data can better track their cash flow, spot inconsistencies, and handle concerns quickly.

This method improves decision-making while reducing the chance of errors that could harm the company’s financial health. ScaleOcean plays an important part in automating the bank reconciliation process, making it more efficient and error-free.

ScaleOcean’s accounting ERP software automates the matching of bank statements with internal records, resulting in rapid and accurate reconciliation while saving businesses time and resources. This streamlined procedure enables firms to focus on strategic initiatives while preserving financial accuracy and compliance. Request a free demo to get this solution for your specific needs.

FAQ:

1. What are the 4 steps in the bank reconciliation?

Bank reconciliation involves four key steps:

1. Compare Statements: Review the company’s cash book and bank statement for discrepancies.

2. Identify Unprocessed Deposits: Spot any deposits not yet processed by the bank.

3. Account for Unprocessed Checks: Record checks issued but not cleared by the bank.

4. Correct Mistakes: Adjust discrepancies in the bank statement or company records.

2. What is the journal entry for bank reconciliation?

Journal entries during bank reconciliation depend on the discrepancies found. Typical entries include:

– Deposits in Transit: No entry is required for these, as they’ve already been recorded in the company’s books.

– Unprocessed Checks: No journal entry is needed unless changes are necessary to the financial records.

– Bank Errors: If a mistake was made by the bank, an entry may be required to correct it.

– Company Errors: If there’s an error in the company’s records, a journal entry is needed to fix the discrepancy.

3. How to reconcile a bank account?

To reconcile a bank account, follow these steps:

1. Collect Documents: Get both the bank statement and the company’s cash book for the same period.

2. Match Transactions: Compare each deposit and withdrawal in the company’s records with those on the bank statement.

3. Spot Differences: Identify any deposits or checks that haven’t been processed or any errors in either record.

4. Make Adjustments: Adjust the company’s ledger to account for any errors, such as bank charges or interest.

5. Calculate Final Balances: Ensure that the final, adjusted balances in both the bank statement and the company’s records match.

4. What is the formula for bank reconciliation?

The bank reconciliation formula is:

Adjusted Bank Balance = Bank Statement Balance + Deposits Not Yet Processed – Unprocessed Checks

For the company’s records:

Adjusted Book Balance = Company’s Cash Book Balance + Bank Mistakes – Company Mistakes

Once all differences are resolved and adjustments made, both adjusted balances should be the same.