Absorption costing is a managerial approach of allocation planning, which allocates all the manufacturing costs, direct labor, direct materials, variable overhead, and fixed overhead to each unit of the product. When the production is greater than the sales, this methodology, which capitalizes the unfixed costs in the form of inventory, and is required to perform the external reporting of the GAAP/IFRS, may overstate the profitability.

This method ensures each product reflects its total cost, offering a comprehensive view of profitability and compliance with financial reporting standards. Singapore’s manufacturing labor cost index was 103.00 in March 2018 (2010 base = 100).

This strategy will ensure that all products capture their total cost to capture a complete picture of profitability and compliance with the financial reporting standards. As of March 2018 (base year = 2010), we have found a report by CEIC Data shows that the manufacturing labor cost index of Singapore was 103.00.

In the context of Singapore in the critical manufacturing sector, the concept of absorption costing will be vital in ensuring effective pricing and cost management, as well as long-term sustainability. In this paper, the concept of absorption costs will be discussed in detail, including the importance of this concept to a manufacturer and how it works in practice.

You will also get the opportunity to learn about its components, how it is differentiated under variable costing, and the benefits and limitations of using the method, or why absorption costing is important in organizations, particularly in the competitive manufacturing industry in Singapore.

- Absorption costing is a method that allocates all manufacturing expenses, including direct materials, labor, and overhead, to each product, ensuring accurate cost allocation.

- Absorption costing works by systematically identifying direct costs, calculating overhead costs, allocating these overheads to products, and determining the full cost per unit.

- Absorption costing provides manufacturers with a complete picture of product costs, helping management make informed decisions based on comprehensive cost structures.

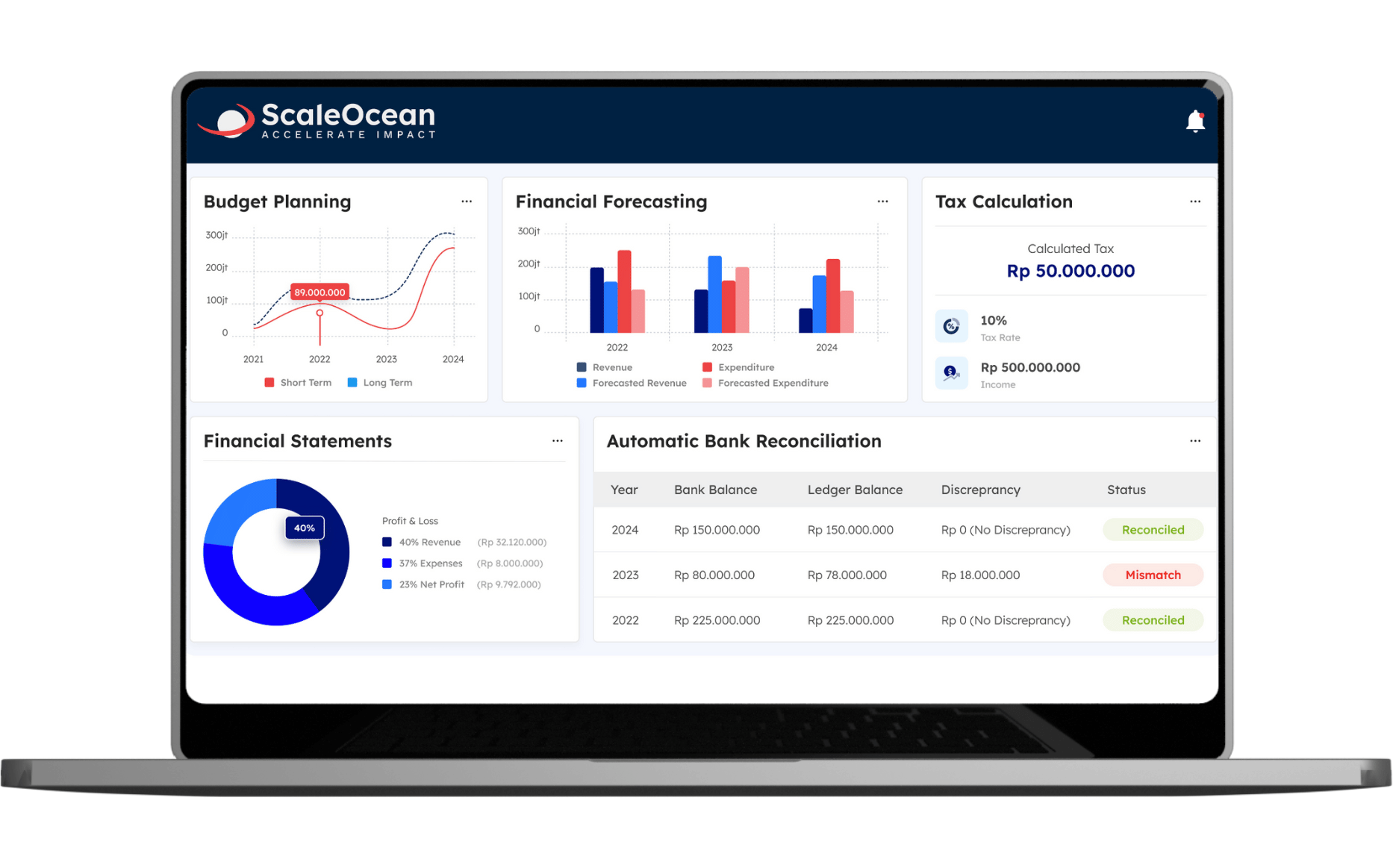

- ScaleOcean, a comprehensive accounting software, replaces inefficient spreadsheets by providing real-time financial visibility, automated processes, and cross-module interaction to improve financial management and decision-making.

What Is Absorption Costing?

Absorption costing, also known as full costing, is a system that allocates all manufacturing expenses to each product. This strategy incorporates direct materials, direct labor, and variable and fixed manufacturing overheads. By using this strategy, producers ensure that each unit produced bears the full burden of production expenses, resulting in a more accurate determination of profitability.

Based on ACRA guidelines, this method aligns with the Singapore Financial Reporting Standards (International), ensuring transparent financial reporting and effective internal controls.

Unlike costing methods that simply include variable expenses, absorption costing includes all production-related costs, providing a complete financial picture. It guarantees that fixed overheads, such as factory rent and equipment depreciation, are considered in inventory valuation and price choices, which aids both financial reporting and internal cost control.

In the end, since there are still some fixed costs in ending inventory, the net income will be larger in absorption costing since the inventory increases (production > sales). Meanwhile, variable costing will show a higher net income when inventory decreases (sales > production).

Absorption Costing Formula

In manufacturing, determining the overall cost incurred by each product unit is crucial for accurate financial reporting and pricing strategies. The absorption costing formula provides a systematic method for capturing all relevant production costs—both direct and indirect—so that no expense is neglected. This strategy enables producers to more precisely allocate expenses among all units produced over a particular period.

Absorption Cost per Unit = (Direct Materials + Direct Labor + Variable Overhead + Fixed Overhead) ÷ Total Units Produced

Using this technique, manufacturers can determine the total cost of each unit, enabling better decisions on inventory, cost control, and profits. It ensures that each product reflects both variable and fixed costs, providing a solid foundation for setting prices and assessing operational efficiency.

Examples of Absorption Costing

To better understand how absorption costing works in manufacturing, consider a real-world example. The absorption costing formula is simple and effective: add direct and manufacturing overhead costs, then divide by units produced. This ensures each unit covers its fair share of production costs, leading to more accurate pricing and inventory valuation.

Absorption Costing Formula: (Direct Materials + Direct Labor + Variable Overhead + Fixed Overhead) ÷ Total Units Produced

For example, consider a manufacturing company generating 1,000 units. The overall expenditures include S$50,000 for direct supplies, S$30,000 for direct labor, S$20,000 for variable overhead, and S$40,000 for fixed overhead. Applying the formula (50,000 + 30,000 + 20,000 + 40,000) ÷ 1,000 yields a unit cost of S$140. This signifies that each product unit has fully absorbed costs of S$140, which is used to calculate inventory valuation and pricing strategies.

Why Use Absorption Costing

Manufacturers use absorption costing to meet financial reporting requirements such as GAAP and IFRS. This strategy ensures that all production-related costs, including fixed overhead, are factored into inventory valuation. As a result, financial statements provide a more accurate and comprehensive picture of industrial processes, in line with regulatory standards.

Absorption costing allows organizations to price products more strategically, safeguard profit margins, and manage total profitability. It prevents underestimating genuine production costs, which could mislead decision-makers.

Reliable external financial reports are also easier to compile, which promotes transparency and credibility in industrial accounting. By integrating this method into your accounting system, manufacturers can ensure more accurate financial data and improve decision-making processes.

Components of Absorption Costing

Absorption costing includes all critical components contributing to the cost of manufacturing a product. Understanding each element is vital for accurate product pricing, inventory valuation, and financial reporting. A recommended manufacturing accounting system in Singapore can streamline these processes for better efficiency.

These components ensure that each unit produced accurately reflects the exact cost incurred, allowing for more informed operational and strategic decisions.

1. Direct Materials

All raw materials that are absorbed directly into the final product during the manufacturing process are considered direct materials. These costs can be easily identified and vary with the level of production. Absorption costing considers direct materials as a high cost and ensures that each unit produced incurs the correct amount of direct material cost.

2. Direct Labor

Direct labor is the expenses of salaries and benefits paid to employees, who are directly engaged in the transformation of raw materials into finished commodities. It is the human labor that is needed to produce each unit. Absorption costing is a costing method that allocates the direct labor per unit produced so that the producers can measure the labor cost contribution to the overall cost of the end product.

3. Variable Manufacturing Overhead

Variable manufacturing overhead is indirect production costs that change with the amount of output, electricity, supplies, etc., for example. These costs are allocated in a proportional manner to all the units. In order to appreciate this, you need to know the manufacturing overhead formula to be able to cost accurately.

4. Fixed Manufacturing Overhead

Fixed manufacturing overhead is used on the expenses that do not change with a change in volume of output, such as lease payments on the factory, depreciation of the equipment, and salaries of the production supervisor. These are expenses borne by all units produced, which reduces the fixed cost per unit as more units are produced.

The importance of including fixed overhead in absorption costing is to ensure that full absorption of the overall resources employed in the manufacturing process is captured. These fixed costs must be handled with caution in the overall context of corporate expense management, where businesses need to maintain an efficient cost structure and financial health.

5. Excluded Cost

Absorption costing does not include any non-manufacturing costs, such as selling, general, and administrative costs. These products are considered period costs and they are expensed immediately on the income statement instead of being charged to the cost of the inventory produced.

How Absorption Costing Works

Absorption costing in manufacturing necessitates a methodical strategy to ensure that all costs are accurately recorded. This strategy assigns direct and indirect costs to products in a systematic manner, benefiting both internal management and external reporting. Manufacturers can fully allocate expenses to each unit produced by following a set of explicit steps, resulting in an accurate reflection of production costs.

1. Identify Direct Costs

The first stage is to identify all direct manufacturing costs, such as raw materials and wages for production workers. These charges are easily traceable to specific items, laying the groundwork for precise cost allocation under absorption costing.

2. Calculate Overhead Costs

Next, manufacturers calculate their variable and fixed production overheads for the accounting period. Variable overheads include indirect materials and factory utilities, while fixed overheads cover factory rent, equipment depreciation, and salaried production personnel. Also, you must learn how to manage overhead costs for better budgeting.

3. Allocate Overheads to Products

Once overhead expenses are calculated, they must be assigned to products in a rational way. Manufacturers often distribute overhead based on machine hours, labor hours, or production units, ensuring that each unit bears its fair amount of indirect costs.

4. Compute Full Cost Per Unit

After determining direct expenses and allocated overheads, producers calculate the total cost per unit. This graph depicts the sum of direct materials, direct labor, variable overhead, and fixed overhead divided by total units produced over time.

5. Value Inventory and Cost of Goods Sold

Finally, inventory and cost of goods sold (COGS) indicators are valued using the full absorption costing approach. This ensures all manufacturing costs are reflected on the balance sheet and income statement, aiding compliance with GAAP and IFRS.

Advantages of Absorption Costing

Absorption pricing gives manufacturers a complete view of product costs, including direct materials, labor, and overheads. This approach ensures each unit reflects the total resources required, offering a more accurate cost picture. As a result, management may make more informed operational decisions based on a comprehensive understanding of cost structures.

Absorption costing helps make better pricing decisions by accurately determining the total cost of production. Using manufacturing cost estimating tools from Singapore, producers can set prices that cover all expenses, achieve desired profit margins, and stay competitive without hidden overheads.

Full absorption costing aligns revenues with all associated expenditures in the same reporting period, which improves financial statement accuracy. This matching approach, similar to accrual accounting, ensures that stakeholders, including investors and auditors, get a clear and reliable picture of the company’s profitability. As a result, it builds stakeholder trust and promotes long-term corporate sustainability.

Among the examples of the advantages, it complies with Singapore Accounting Standards. The Singapore Financial Reporting Standards (SFRS) require all manufacturing costs to be allocated to the products, underlying its adherence to absorption costing. This makes it able to comply with financial reporting requirements.

Disadvantages of Absorption Costing

Despite its benefits, absorption costing can cause manufacturers to misread cost behavior, particularly when examining internal efficiency. This misconception can make it difficult to discern between variable and fixed costs, thereby influencing strategic decisions in industrial operations. Over time, this can lead to inefficiencies that lower a company’s overall competitiveness.

Because fixed expenses are shared across all units, low production quantities might artificially raise unit costs. When production output declines, per-unit costs rise, distorting profitability calculations and leading to bad pricing strategies if not carefully handled. Manufacturers must regularly monitor seasonal demand swings to avoid pricing themselves out of the market.

Furthermore, depending entirely on full costing may mask cost management methods, making it difficult to discover waste or inefficiencies. Manufacturers may struggle to optimize processes and save costs without visibility into controllable expenses at different production stages. This lack of openness can stymie efforts to apply lean manufacturing principles successfully.

Less suitable for costing individual products, especially when production volumes vary, is one of the examples of the disadvantages. This may affect the pricing moves of businesses that have different levels of production, such as electronics manufacturers in Singapore.

Absorption Costing vs. Variable Costing

The major difference between absorption costing and variable costing is how they handle fixed production overheads. Absorption costing assigns all fixed overhead costs to each unit produced, thereby including them in the product’s total cost.

This method ensures that inventory values on the balance sheet reflect both variable and fixed manufacturing costs, as required for GAAP and IFRS reporting. These costs are also recorded in the general ledger, ensuring consistency in financial reporting across all accounting records.

Variable costing, on the other hand, treats fixed production overheads as period expenses, which are recognized promptly in the income statement. This strategy provides manufacturers with a clearer picture of how production quantities affect profitability by isolating variable expenses per unit.

While absorption costing is useful in statutory reporting, variable costing is frequently chosen internally for operational analysis and short-term decision-making. To help you get a better understanding, here are the differences between absorption costing and variable costing:

| Feature | Absorption costing | Variable costing |

|---|---|---|

| Treatment of fixed MOH | Included as product cost (inventory) | Treated as a period cost (expensed immediately) |

| Formula | DM + DL + VOH + FMOH | DM + DL + VOH |

| Inventory valuation | Higher (including fixed overhead) | Lower (only included variable costs) |

| Financial reporting | Required for external reporting (GAAP/IFRS) and tax | Used for internal management and decision-making |

| Impact of production | Net income will be larger in absorption costing since the inventory increases (production > sales) | Variable costing will show a higher net income when inventory decreases (sales > production) |

Use Comprehensive Accounting Software ScaleOcean Instead of Time-Wasting Spreadsheets

ScaleOcean manufacturing ERP provides an accounting system that helps manufacturers streamline their financial processes. It provides real-time financial visibility, automated accounting processes, and seamless cross-module interaction, hence removing the inefficiencies of manual spreadsheets.

ScaleOcean enables manufacturers to maintain accurate, timely, and audit-ready financial records, allowing them to make better business decisions faster.If you want to increase financial accuracy, operational efficiency, and make faster, wiser decisions in your manufacturing business.

ScaleOcean provides a free demo to help you discover its full potential. Furthermore, Singapore-based manufacturing enterprises can take advantage of the CTC grant up to 70% of funding to reduce implementation costs and increase ROI. The following are the primary USPs of ScaleOcean software:

- Real-Time Financial Visibility & Smooth Cashflow: ScaleOcean delivers up-to-date financial data, allowing businesses to track cash, payables, receivables, and inventory in real time.

- Efficiency in Calculation & Automated Accounting: Revenue, cost, profit, and tax calculations are fully automated, minimizing errors and speeding up transaction recording.

- Automated Bank Reconciliation: Bank reconciliation becomes faster and more accurate, significantly reducing manual matching errors.

- Comprehensive Financial Reporting with SFRS Compliance: Financial reports generated are SFRS-compliant, audit-ready, and support better strategic decisions.

- Strong Cross-Module Integration: The accounting module integrates with sales, inventory, asset, and revenue management systems, eliminating the need for double manual data entries.

Conclusion

Absorption costing helps manufacturers capture the total cost of production, improving inventory valuation and compliance with financial reporting rules. By understanding its workings and components, manufacturers can make better pricing and operational decisions. This leads to long-term profitability. While absorption costing has several benefits, maintaining it manually using spreadsheets can be time-consuming and error-prone.

ScaleOcean provides a comprehensive accounting system designed specifically for manufacturing to help you simplify and optimize your financial processes. Our solution automates real-time cash flow tracking and SFRS-compliant reporting, letting you focus on growing your business without the headache of spreadsheets.

Request a free demo today and learn how ScaleOcean can improve your finance management efficiency and accuracy.

FAQ:

1. What is meant by absorption costing?

Absorption costing, or full costing, is a method where all manufacturing expenses, including direct materials, direct labor, and both variable and fixed overheads, are assigned to the products being made. This method ensures that each product’s cost includes the total production expenses, offering a comprehensive view of financial performance.

2. What is the difference between absorption costing and standard costing?

Absorption costing allocates actual production costs to products, incorporating both fixed and variable overheads. In contrast, standard costing uses predetermined estimates based on historical or projected data for direct materials, labor, and overhead. The key distinction is that standard costing relies on estimated costs, while absorption costing is based on actual expenses.

3. What is absorption costing and marginal costing?

Absorption costing includes all production-related expenses, both fixed and variable, in the product cost, making it a more complete costing method. Marginal costing, however, only considers variable production costs in the product’s cost, treating fixed expenses as period costs. The main difference lies in the treatment of fixed costs in the cost structure.

4. What is the absorption pricing method?

The absorption pricing method involves setting a product’s price to cover the full production cost, which includes direct costs as well as variable and fixed overheads. This ensures that the product price reflects the total expenses involved in its production, helping businesses ensure their pricing covers all costs and generates profit.