The accounting cycle is a systematic method used by firms to record, classify, and summarize financial transactions over a set time period. This cycle assures accurate financial reporting, aids in compliance with accounting rules, and provides vital insights into a company’s financial health.

In Singapore, businesses benefit from the flexibility in choosing their fiscal year-end (FYE) date. According to InCorp Global, companies can select their own FYE date, as long as it complies with legal requirements and remains consistent year after year.

This flexibility allows businesses to align their accounting cycle with their operational cycles, making financial planning and reporting more effective. This article will look at the accounting cycle, its essential components, and how they play an important role in a firm’s financial management, particularly in Singapore.

We will go over each 8 phases of the accounting cycle, from transaction identification and analysis to financial statement generation, and we will highlight effective practices for increasing accounting cycle efficiency. We will also look at how excellent accounting software can help to speed up this process and ensure accuracy.

- The accounting cycle is a multistep process used by firms to record, categorize, and summarize financial statements.

- For business owners, understanding the importance of the accounting cycle helps ensure financial records are accurate and up-to-date, leading to better financial performance monitoring.

- The accounting cycle consists of several key steps, from identifying transactions to generating financial statements, each critical for ensuring financial transparency and compliance.

- ScaleOcean’s best accounting software provides a comprehensive accounting solution that maximizes corporate efficiency through automation and seamless connectivity.

What Is the Accounting Cycle?

The accounting cycle is a repeatable process used by firms to record, categorize, and summarize financial statements. This eight cycle guarantees that all financial actions are carefully tracked, allowing organizations to assess their financial success over time.

By following a structured approach, businesses can keep their financial records organized, which is key for transparency, reporting, and staying compliant with regulations. It helps track revenues, expenses, assets, and liabilities while ensuring accuracy and gaining stakeholder trust.

The goal of the accounting cycle is to provide clear and precise financial reports, which are essential for making smart business decisions. It lets companies generate reliable reports at the end of each period, helping owners, managers, and investors make better-informed choices.

The Importance of the Accounting Cycle for Business Owners

The accounting cycle is important for business owners to grasp to ensure that their financial documentation is well-kept and accurate. They can perform and make better decisions when they follow the steps of recording transactions to preparing financial statements.

Accrual accounting makes this a bit easier by matching revenues with expenses with the actual production of those goods, rather than when compensation is received through cash transactions. In this way, owners can enjoy better resource management, control over money matters, and benefit the business for growth and long-term stability.

At the end of the accounting cycle also means that businesses will be able to maintain control over their finances, as well as not be penalized for not following the provisions of financial regulations. Owners should check these financial numbers on a regular basis to identify trends, make better choices, and avoid financial surprises to help ensure that their company is successful.

The Steps in the Accounting Cycle

The accounting cycle consists of many essential steps that facilitate the proper, accurate, and timely documentation, classification, and reporting of financial transactions. The key steps in any cycle are essential for financial transparency, compliance, and providing business leaders with the information to make informed decisions.

Here are the explanations for the accounting cycle and its importance in the field of accounting:

1. Identifying and Analyzing Business Transactions

The initial step of an accounting cycle is to recognize and analyze key financial transactions occurring within the company. These deals may include buying or selling, investing,g or costs.

Purchase journals are a typical means of business bookkeeping for those making purchases on credit because they are able to accurately track and record those purchases. Through the knowledge of these transactions, organizations can correctly assign the transactions to the relevant accounting processes in the future.

This is an important stage because it has the potential to influence all subsequently performed accounting tasks.

2. Recording Journal Entries

Double-entry bookkeeping is a method that is used by businesses to document a transaction once they have been identified. Debits and credits have two sides of the transaction that help balance the accounting equation Assets = Liabilities + Equity.

It yields a distinct and sequential ledger of financial transactions. These journal entries are made by businesses to ensure that their financial records are accurate and complete.

3. Posting to the General Ledger

Once journal entries are made, they are entered into the general ledger, which serves as a summary of all accounts. The general ledger is where all transactions from many accounts will be compiled in one record to get an overall financial status of the business.

This helps to track and monitor financial operations in various financial sectors, making it structured.

4. Preparing an Unadjusted Trial Balance

The unadjusted trial balance is used to make sure that the number of debits corresponds to the number of credits and may be added in the trial balance before any adjustments are made.

This phase is useful for the discovery of any errors made during recording and can give an overview of a company’s current financial position. This is done as an early checking process to make sure accuracy of records before any other changes are carried out.

5. Making Adjusting Entries

Adjusting entries are made to put the company’s financial records in a state that is true and fair in accordance with the company’s financial position. These changes can involve recognition or deferral of receipts or payments that were already reported, or even revisions to previous transactions.

The accuracy of the entries ensures the financial statements are accurate and reflect the business’s actual performance.

6. Preparing Adjusted Trial Balance

Once firms make the necessary adjustments, they make an adjusted trial balance. During this stage, all accounts are balanced, and the books are corrected so that there is an accurate record.

It helps as a starting point to develop accurate financial statements and as a last chance inspection before publication of Reports.

7. Generating Financial Statements

The next step of the accounting cycle is the financial statements. These comprise an income statement, balance sheet, and cash flow statement, all of which give information about the company’s profit margin formula, assets, liabilities,s and cash flow.

These are essential for decision-making and providing the company with financial information to stakeholders.

8. Closing the Books

Finally, the Accounting Dept. seals the books at the end of each accounting period. Temporary accounts (revenue accounts, expense accounts) are closed to zero to start the next period of accounting.

This ensures that the financial reporting cycle starts afresh, which gives another fresh look at the financial transactions for the next reporting period.

Key Benefits of the Accounting Cycle

The accounting cycle is crucial to maintaining and ensuring the honesty and accuracy of financial records. Taking a step-by-step and organized approach helps businesses ensure transparency, timely reporting, and compliance with all regulations for success.

Here are the essential advantages of the accounting cycle:

- Improved Accuracy and Reliability: Accounting Cycle provides a proper record of all financial transactions, resulting in accurate and reliable financial statements. This minimizes mistakes and keeps your financial information up to date,e reflecting the actual position of the business.

- Efficient Processes: Automated processes and streamlined methods help save time and eliminate manual work in the accounting cycle. This will boost data input, reduce the likelihood of errors, and enable your staff to concentrate on strategic tasks without the need to worry about financial admin.

- Better Compliance: The accounting cycle keeps businesses in check with local necessities and global norms. It ensures that financial reports are always current and accurate, minimising the risk of fines and enabling transparency in financial reporting.

- Real-time business financial performance up to the minute: Adopting an accounting cycle helps businesses understand their real-time financial performance. It allows them to monitor the revenue generated, costs involved,d and profitability numbers, which are essential to comprehend the performance of the business.

- Enables Better Decision Making: The accounting cycle ensures that decision makers have accurate and timely financial information available. This assists them in making wise decisions when it comes to budgeting, allocating resources, and planning for the future in order to make sure that the business is on course.

- Covers Consistency in Financial Planning and Analysis: Fund management and accounting will provide you with reliable data for planning and analysis. It helps in establishing realistic targets, predicting future performance better, and streamlining finances to suit the company’s goals.

The components of the accounting cycle enable businesses to maintain accuracy, efficiency, compliance, and insightful decision-making. With ScaleOcean ERP, this can be simplified through automation, real-time data integration, and consistency, boosting business efficiency.

Accounting Cycle vs. Budget Cycle

The Accounting Cycle and the Budget Cycle are both essential for managing a business’s finances. While they each have different focuses, they work together to support financial stability and long-term growth. Understanding their roles helps businesses make smarter decisions.

Here’s a comparison table to help you see the key differences between the Accounting Cycle and the Budget Cycle:

| Feature | Accounting Cycle | Budget Cycle |

|---|---|---|

| Purpose | Tracks and records past financial activities. | Prepares and projects future financial needs. |

| Focus | Reflects actual performance (revenue, expenses, obligations). | Assists in resource allocation, setting goals, and forecasting. |

| Timeframe | Reflects the past (historical data). | Looks ahead (future planning and forecasting). |

| Function | Ensures accurate reporting and compliance. | Enables financial development and future planning. |

| Key Activity | Recording revenue, expenses, and obligations. | Allocating resources, setting goals, and forecasting spending. |

When Do You Time the Accounting Cycle Correctly?

To keep consistent and accurate financial records, organizations must time their accounting cycles correctly. Typically, the accounting cycle corresponds to the business’s fiscal period, which might be monthly, quarterly, or annual.

According to Osome, a fiscal year is a 12-month period that a company selects to report its financial information. Each cycle provides a defined timeframe for tracking transactions, making adjustments, and preparing financial statements that appropriately reflect the company’s performance.

The accounting cycle starts and finishes within an accounting period, which is when financial statements are prepared. The length of the period varies, with the most common being an annual period, although businesses with complex processes may opt for quarterly cycles.

Regardless of the frequency, completing the cycle within the specified timeframe ensures timely and trustworthy financial reporting, allowing businesses to make educated decisions based on current information.

How to Enhance Efficiency in Your Business’s Accounting Cycle?

Long-term business performance and improved financial management depend on your accounting cycle being more efficient. In addition to guaranteeing accuracy, a streamlined accounting procedure saves your business money and time.

Businesses can reduce human errors, enhance decision-making, and streamline their financial operations by implementing best practices and utilizing the appropriate tools.

Timely, accurate financial data enables businesses to react faster to market fluctuations and make better-informed decisions through an effective accounting cycle. The following recommended practices will help you streamline and improve the effectiveness of your accounting process:

Automate Key Accounting Processes

Automating journal entry recording and ledger posting helps increase accuracy and reduce human error. The entire process is accelerated by automation, freeing up your team to concentrate on strategic decision-making rather than mundane duties.

This guarantees a more efficient accounting process and lessens the requirement for ongoing human supervision.

Implement a Centralized Accounting System

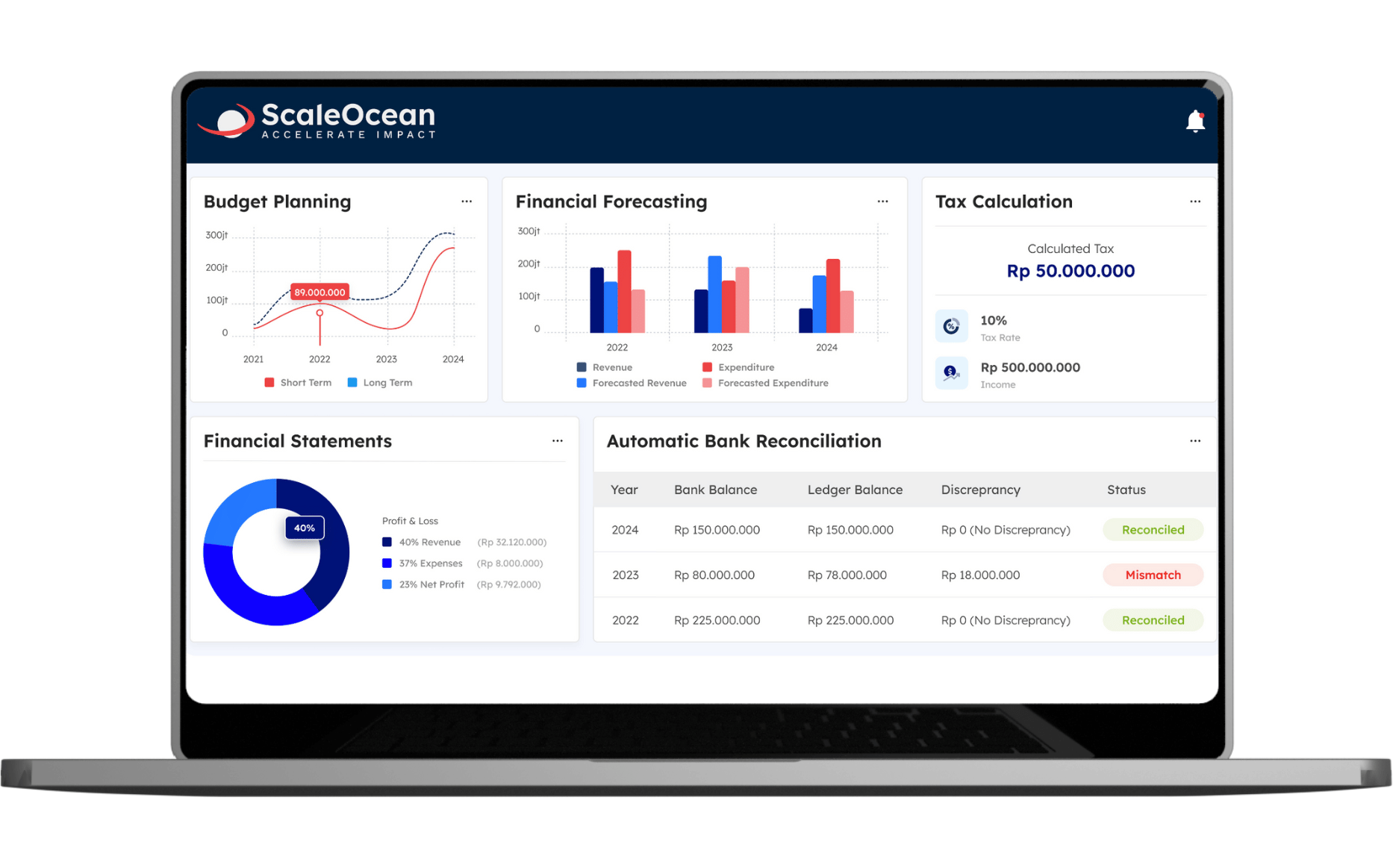

A centralized accounting system consolidates all financial data onto a single platform, enhancing communication and removing silos. ScaleOcean’s cloud-based platform makes financial data tracking easier, saves duplication, and improves transparency.

ScaleOcean improves real-time decision-making, cooperation, and compliance by centralizing financial activities, resulting in an optimized accounting cycle.

Regularly Review Financial Statements

Conduct regular checks of your financial statements to ensure accuracy and catch any irregularities early on. This approach aids in making educated decisions, spotting trends, and ensuring that your company remains financially stable.

Staying proactive with these reviews allows you to address possible issues before they become serious difficulties.

Utilize Cloud-Based Accounting Software

Cloud-based accounting software, such as ScaleOcean, connects effortlessly with your current business systems. It improves financial transparency, lowers manual errors, and accelerates the accounting cycle, giving you real-time financial data.

ERP financial accounting software also provides remote access, allowing you to manage your funds from anywhere and at any time.

Ensure Compliance and Accuracy

Update your accounting processes on a regular basis to ensure that you are in compliance with the current financial requirements and standards. Using software that automatically updates regulations ensures accuracy and prevents penalties for noncompliance.

This helps your company stay compliant with local and international regulations, reducing the risks connected with financial reporting.

Streamline the effectiveness of the Accounting Cycle Process with ScaleOcean

ScaleOcean’s best accounting software is an all-in-one accounting solution that increases the effectiveness of companies by automating their job and guaranteeing a smooth combination. The programme makes certain accounting procedures easy, which helps organizations better manage their financial procedures, lower error rates, and save time.

By streamlining its accounting cycles, enhancing financial decision-making, and ensuring regulatory compliance, ScaleOcean’s powerful capabilities allow businesses to reduce costs and optimize their financial processes. A flexible and agile solution, ScaleOcean is a good choice for any-sized business.

Take advantage of a demo of ScaleOcean’s accounting software and discover how it can transform your accounting. Singapore’s CTC grant, up to 70% of funding, is also available for ScaleOcean to be scaled up, allowing businesses to reduce implementation costs and also simplify accounting processes in doing so.

Here are some of ScaleOcean’s most valuable distinctive features:

- Customizable Accounting Solutions: ScaleOcean lets you personalize accounting systems, including automated entries and department-specific settings for better efficiency.

- Effortless Integration Across Branches: ScaleOcean seamlessly integrates accounting functions across branches, centralizing data for smooth collaboration.

- Automated Journal Entries and Ledger Posting: ScaleOcean automates journal entries and ledger postings, reducing human error and ensuring timely, accurate financial updates while freeing up time for strategic tasks.

- Real-Time Financial Reporting: ScaleOcean provides real-time financial reporting, giving businesses up-to-date insights to make smarter decisions and quickly respond to market changes.

- Ensuring Compliance and Accuracy: ScaleOcean ensures compliance with local laws like Singapore Accounting Standards (SFRS) and keeps financial reporting accurate to avoid regulatory fines.

Conclusion

The accounting cycle is important to provide accurate and efficient financial management. Each phase, from transaction recognition through to the creation of financial statements, can help ensure businesses keep accurate records, provide informed decision-making, and meet regulations.

ScaleOcean accounting software is a complete solution, improving all aspects of the accounting cycle. With its cloud-based software, it is able to automate important tasks, guarantee adherence, and deliver real-time financial information all within a single platform that is customisable for your organization.

Schedule a free demo today to find out how ScaleOcean can benefit your accounting business and help your company succeed.

FAQ:

1. What are the 5 basic accounting cycles?

The five essential stages in the accounting cycle are recording transactions, posting them to the ledger, preparing an unadjusted trial balance, making necessary adjustments, and generating financial statements. These steps ensure thorough and accurate financial reporting.

2. What is the big 5 in accounting?

Though now referred to as the Big Four, there was once a “Big Five.” Arthur Andersen, once a leader in the accounting industry, was a prominent member of this group, alongside PwC, Deloitte, EY, and KPMG, known for their excellence in the field.

3. What is the IAS 10 in accounting?

IAS 10 outlines guidelines for adjusting financial statements based on events that occur after the reporting period. It also specifies the disclosures businesses must make about the authorization date of the financial statements and any subsequent events.

4. What is the 4 4 5 accounting system?

The 4–4–5 system is a method of structuring accounting periods, commonly used in industries like retail and manufacturing. It divides the year into four quarters of 13 weeks, with each quarter consisting of two 4-week months and one 5-week month.