Goods and Services Tax is a consumption-based tax applied to most goods and services supplied in Singapore, calculated at each stage of the transaction. It directly impacts pricing, compliance, and reporting accuracy across industries and operations.

Moreover, businesses must manage goods and services tax GST carefully because errors can quickly compound across invoices, returns, and financial records. Without structured processes, companies often struggle to maintain consistency, especially when handling large transaction volumes daily.

However, a critical pain point is the risk of compliance issues and financial penalties arising from incorrect GST reporting. Miscalculations, inaccurate declarations, or missing GST components in pricing can trigger audits and costly fines for businesses.

Therefore, implementing an accurate GST system is essential for automating calculations, validating transactions, and generating compliant reports. With strong internal controls, businesses reduce audit risks while ensuring consistent, reliable financial reporting aligned with regulatory requirements.

In this article, we will understand how GST works, which transactions are taxable, how reporting obligations apply, and how to perform the goods and services tax calculator accurately. In doing so, it helps you strengthen compliance while improving your financial and operational efficiency.

- Goods and services tax is a consumption-based tax that affects pricing, compliance, reporting accuracy, and financial operations across businesses in Singapore.

- Taxable and non-taxable supplies require correct GST classification to ensure accurate reporting, compliance management, and proper input tax treatment.

- Charging and claiming GST requires accurate invoice documentation, proper tax allocation, and careful reconciliation between output and input taxes.

- GST calculations involve applying tax rates to taxable supplies and deducting eligible input tax from the output tax collected.

- ScaleOcean Accounting Software helps businesses automate GST calculations, improve compliance accuracy, simplify reporting, and streamline financial management processes.

What Is the Goods and Services Tax (GST)?

The Goods and Services Tax is a broad-based consumption tax applied to most supplies of goods and services in Singapore. It is collected by businesses at each stage of the transaction and ultimately borne by end consumers.

Additionally, goods and services tax GST operates as a value-added tax, meaning businesses charge GST on sales and claim credits on purchases. This mechanism ensures tax applies only to value added, improving neutrality across industries and transactions.

However, businesses must manage GST carefully because incorrect classification or reporting can create compliance gaps. These issues often lead to reconciliation challenges, financial discrepancies, and increased administrative burden during reporting periods.

Therefore, companies adopt structured GST processes and systems to ensure accurate goods and services tax calculations, proper documentation, and timely submissions. This approach supports compliance while maintaining financial transparency and operational efficiency.

Taxable and Non-Taxable Goods and Services

Businesses must distinguish between taxable and non-taxable supplies to ensure correct goods and services tax GST treatment. Each category carries different implications for pricing, reporting, and input tax claims, making classification a critical operational requirement.

Moreover, incorrect classification can result in underpayment or overpayment of GST, affecting both compliance and profitability. Therefore, understanding these categories helps businesses align their processes with regulatory expectations and avoid unnecessary risks.

Taxable Supplies

Taxable supplies include goods and services subject to GST at either the standard or zero rate. Businesses must charge GST accordingly, maintain documentation, and report transactions accurately within prescribed filing deadlines.

Furthermore, taxable supplies require businesses to monitor GST registration thresholds and ensure timely filing with IRAS (Inland Revenue Authority of Singapore). Proper classification between standard-rated and zero-rated supplies ensures accurate tax treatment and avoids compliance issues.

Comparison Table: Taxable Supplies

| Type | Standard-Rated Supplies (9% GST) | Zero-Rated Supplies (0% GST) |

|---|---|---|

| Goods | Most local sales, including retail items and imported low-value goods. Register if revenue exceeds S$1M. File GST returns quarterly, typically one month after each accounting period ends. | Export of goods shipped overseas. Registration threshold remains S$1M. Filing deadlines align with standard GST reporting cycles, and supporting export documentation is required for compliance. |

| Services | Local services such as consulting or spa services, including imported services under reverse charge. Registration applies above S$1M turnover, with quarterly filing obligations aligned to IRAS schedules. | International services such as overseas transport or cross-border services. Registration threshold remains consistent, and businesses must retain proof to justify zero-rating during audits and reporting reviews. |

Non-Taxable Supplies

Non-taxable supplies include exempt supplies, which are specifically listed in the GST Act, and out-of-scope transactions where GST does not apply. These categories affect input tax recovery and require careful tracking to ensure accurate financial reporting and compliance.

In addition, businesses must clearly separate these supplies from taxable transactions to avoid incorrect GST claims. Misclassification can affect input tax recovery and lead to issues during audits or financial reconciliations.

Comparison Table: Non-Taxable Supplies

| Type | Exempt Supplies (GST is not applicable) | Out-of-Scope Supplies (0% GST) |

|---|---|---|

| Goods | Includes the sale or rental of unfurnished residential property and investment in precious metals. Businesses exceeding S$1M must register but cannot claim input tax in full. Filing follows standard GST deadlines. | Goods supplied entirely outside Singapore, such as overseas-to-overseas sales. No GST applies, but businesses must still assess registration thresholds and maintain records for reporting clarity. |

| Services | Financial services and digital payment tokens, such as cryptocurrency exchanges. Registration applies above S$1M, but input tax claims are restricted. Filing deadlines remain aligned with IRAS requirements. | Private or non-business transactions outside the GST scope. These do not attract GST, yet businesses must document them properly to ensure accurate classification and avoid reporting inconsistencies. |

Why Governments Use GST

Governments implement GST to create a stable and predictable revenue stream while minimizing economic distortion. Because GST applies broadly, it distributes the tax burden across consumption rather than income or corporate profits.

Additionally, GST enhances transparency because it is clearly reflected in pricing and invoices. This visibility allows governments to monitor compliance effectively while encouraging businesses to maintain accurate transaction records and reporting practices.

Moreover, GST supports economic neutrality by treating most goods and services consistently. This approach reduces market distortions and allows businesses to compete fairly without significant tax-driven pricing differences across sectors.

Therefore, GST systems often integrate digital reporting and compliance frameworks to improve efficiency. These systems help governments streamline tax collection while enabling businesses to automate goods and services tax calculations, manage their Tax Identification Number (TIN), and reduce administrative complexity.

Businesses Required to Register for GST

Businesses must register for GST when their taxable turnover exceeds S$1 million over a 12-month period. This requirement ensures that companies contributing significantly to the economy participate in the tax system.

Additionally, businesses expecting to exceed this threshold soon must register in advance. Early registration helps avoid penalties while ensuring that systems and processes are prepared to handle GST collection and reporting requirements.

However, voluntary registration is also available for businesses below the threshold. This option benefits companies seeking input tax recovery, although it introduces additional compliance responsibilities and reporting obligations.

Therefore, companies must evaluate their financial position, transaction volume, and operational readiness before registering. A structured approach ensures compliance while minimizing disruptions to existing financial and operational workflows.

Charging and Claiming GST

Charging and claiming GST involves collecting tax on sales and recovering tax on purchases. Businesses must apply the correct rates, maintain invoices, and ensure proper documentation for all transactions during reporting periods.

Moreover, accurate processes reduce discrepancies between output and input tax, ensuring smoother reconciliation. Businesses that implement automation often improve accuracy while reducing manual errors and compliance risks.

Charging GST

Businesses charge GST on taxable supplies based on the applicable rate, whether standard or zero-rated. They must issue tax invoices, display GST-inclusive pricing, and ensure accurate calculations across all transactions.

Additionally, companies must report the GST collected in their periodic returns and submit payments to IRAS by the deadlines. Strong internal controls help prevent underreporting, which could otherwise result in penalties or audits.

Claiming GST

Businesses can claim input tax on purchases used for taxable supplies, provided they maintain valid documentation. This includes supplier invoices, import permits, and records that clearly support the GST incurred.

However, input tax claims are restricted to exempt supplies, requiring careful allocation methods. Therefore, many companies adopt the best tax software in Singapore to improve compliance accuracy, automate tax allocation, and reduce reporting errors.

How to Pay the Output Tax and Claim the Input Tax

Businesses pay output tax by collecting GST on taxable sales and reporting it in periodic GST returns submitted to the Inland Revenue Authority of Singapore. They must reconcile invoices, ensure accuracy, and meet strict filing deadlines.

Additionally, companies must pay the net GST payable after offsetting input tax. Timely payment prevents penalties, while consistent reconciliation ensures financial accuracy across reporting periods and reduces risks of audit discrepancies.

To claim input tax, businesses must retain valid tax invoices, import permits, and supporting documentation. These records prove that GST was incurred on purchases used for taxable business activities and that eligible claims were made.

However, businesses cannot fully claim input tax on exempt supplies, so careful allocation is required. Therefore, structured accounting systems help track eligibility, ensure compliance, and support accurate reporting during audits or financial reviews.

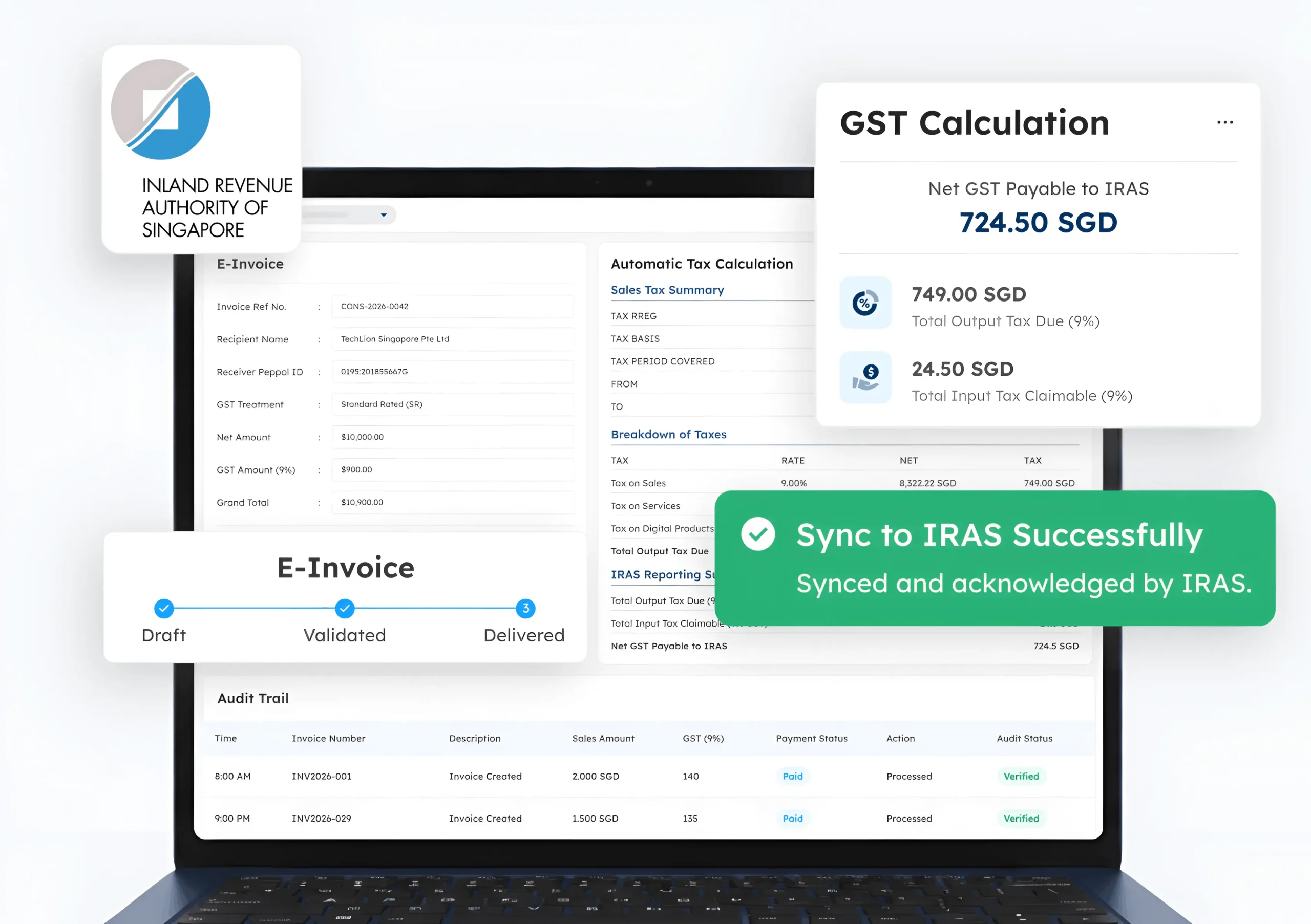

So businesses can use systems such as ScaleOcean Accounting Software, which helps them manage GST reporting, input tax allocation, and financial reconciliation on a single, integrated platform. By automating transaction recording and tax calculations, companies can reduce manual errors while improving compliance accuracy.

Additionally, the system provides real-time financial visibility, automated report generation, and IRAS-ready documentation to simplify audits and regulatory reviews. With centralized accounting processes, businesses can manage taxable and exempt supplies more efficiently while maintaining accurate and transparent financial records.

Case Study Goods and Services Tax

Compliance with the goods and services tax in Singapore directly impacts corporate operations, especially for multinational companies. For example, Infosys faced penalties from IRAS for GST payment issues, highlighting that even large firms can encounter compliance risks.

Moreover, the goods and services tax in Singapore collected billions in GST revenue annually, demonstrating its importance to national finances and the strict enforcement environment. Businesses must therefore maintain accurate reporting systems to operate effectively within this regulatory framework.

In India, the implementation of GST demonstrates both the scale and complexity of a large economy. The country unified multiple indirect taxes into a single system, improving transparency while maintaining a multi-stage, consumption-based tax structure.

For example, India’s GST collections reached trillions of rupees annually, reflecting strong economic activity and compliance expansion. You can find additional details in the India GST collection report, which emphasizes steady growth in tax revenue.

Additionally, companies in India face enforcement actions for non-compliance. Cases involving tax demands and investigations demonstrate how authorities actively monitor GST reporting and enforce regulations to maintain system integrity.

Goods and Services Tax vs. Generation-Skipping Transfer Tax

GST differs significantly from the generation-skipping transfer tax because each serves distinct purposes within taxation systems. While GST applies to consumption, the generation-skipping transfer tax focuses on wealth transfers across generations.

Moreover, GST applies continuously to business transactions, whereas the generation-skipping transfer tax applies only in specific inheritance or estate-planning scenarios. This distinction affects compliance, frequency, and reporting requirements.

| Aspects | Goods and Services Tax | Generation-Skipping Transfer Tax |

|---|---|---|

| Purpose | Tax on consumption of goods and services | Tax on wealth transfer across generations |

| Application | Applied to sales transactions | Applied to inheritance or gifts |

| Frequency | Ongoing, transaction-based | Occasional, event-based |

| Payer | End consumer, collected by businesses | An individual transferring wealth |

| Scope | Broad, applies to most goods and services | Narrow, applies to specific estate transfers |

| Regulatory Authority | Tax authorities like IRAS | Tax authorities governing estate taxes |

Who Has to Pay GST?

Businesses registered for GST must collect and remit tax on taxable supplies. This obligation applies once annual taxable turnover exceeds S$1 million, ensuring that larger economic participants contribute to the tax system.

Additionally, consumers ultimately bear GST because it is included in final prices. Businesses act as intermediaries, collecting and transferring tax to authorities while maintaining compliance with reporting requirements.

However, certain businesses voluntarily register for GST to claim input tax credits. This strategy benefits companies with high taxable purchases, although it increases administrative responsibilities and compliance obligations.

Therefore, companies must assess whether registration is mandatory or beneficial. Proper evaluation ensures alignment with financial goals while maintaining regulatory compliance and operational capacity.

How Is GST Calculated?

GST is calculated as a percentage of the taxable value of goods or services supplied. Businesses multiply the applicable GST rate by the selling price to determine the tax amount charged to customers.

Additionally, businesses compute net GST payable by subtracting input tax from output tax. This mechanism ensures that only the value added at each stage of the supply chain is taxed.

For example, a business sells services worth S$1,000 at Singapore’s standard GST rate of 9%, so the output tax is 1,000 × 9% = S$90. The total invoice amount then becomes 1,000 + 90 = 1,090. If the business already paid S$40 as input tax on purchases, the net GST payable to IRAS becomes: 90 − 40 = S$50

Therefore, accurate calculation requires proper classification of supplies, correct application of rates, and consistent recordkeeping. Errors in any step can lead to compliance issues and financial discrepancies.

Are VAT and GST the Same?

VAT and GST are fundamentally similar because both are consumption-based taxes applied at each stage of the supply chain. They rely on input and output tax mechanisms to avoid double taxation.

However, differences exist in terminology, structure, and implementation across countries. Some jurisdictions use VAT systems with multiple rates, while others adopt GST with simpler or unified structures.

Moreover, GST often emphasizes a streamlined tax system, for the goods and services tax in Singapore. Whereas VAT systems in other regions may involve more complex regulatory frameworks and variations in their application.

Therefore, while VAT and GST share core principles, businesses must understand local regulations to ensure compliance. Misinterpreting these differences can lead to incorrect tax treatment and reporting errors.

Automatically calculate GST with ScaleOcean

ScaleOcean Accounting Software helps businesses automate GST calculations through an all-in-one system that efficiently manages financial data, reporting, and compliance. By centralizing processes, companies reduce manual errors while ensuring accurate tax calculations across transactions.

Additionally, ScaleOcean offers integrated modules that track revenue, expenses, and GST obligations in real time. These features simplify monitoring while ensuring businesses maintain accurate records aligned with Singapore’s tax reporting requirements.

The system also provides flexible customization, enabling companies to adapt GST configurations in response to regulatory updates and business needs. This adaptability ensures long-term compliance while supporting operational changes without disrupting financial workflows.

Importantly, ScaleOcean qualifies for the CTC grant, allowing businesses to access up to 70% in funding support. This makes implementation more affordable while helping companies upgrade their GST processes with a cost-efficient, scalable solution.

Key Features of ScaleOcean Accounting Software:

- IRAS e-Tax Integration: Connect directly with IRAS myTax Portal to streamline GST submission processes, reduce manual errors, and ensure faster, more accurate online tax reporting.

- Automated Tax Code Mapping: Automatically assign correct tax codes such as standard-rated, zero-rated, or exempt supplies, ensuring every transaction follows GST classification rules without manual intervention.

- GST F5 Report Generation: Automatically generate GST F5 return drafts from transaction data, allowing businesses to review figures before submission and improve reporting accuracy each quarter.

- Tax Invoice and Receipt Issuance: Create compliant invoices with GST registration numbers and detailed tax breakdowns, ensuring customers can validate transactions and claim input tax without documentation issues.

- GST Audit File (IAF) Export: Export transaction data to the IRAS Audit File format to simplify audit preparation and make it easier to provide required documentation during regulatory reviews or inspections.

- Input and Output Tax Management: Track and calculate the difference between collected output tax and paid input tax, helping businesses efficiently determine the exact GST payable or refundable.

- Multi-Currency GST Handling: Automatically convert foreign-currency transactions into SGD at official exchange rates, ensuring accurate GST treatment for international and cross-border transactions.

- Scalable Tax Configuration: Update GST rates and tax rules within the system when regulations change, ensuring long-term compliance without requiring major system overhauls or operational disruptions.

Conclusion

Goods and services tax plays a critical role in business operations because it affects pricing, reporting, compliance, and financial accuracy. Therefore, businesses must understand GST classifications, calculations, registration requirements, and reporting obligations to reduce risks while maintaining operational efficiency and regulatory compliance.

ScaleOcean Accounting Software helps businesses automate GST calculations, manage tax codes, generate GST F5 reports, and maintain accurate financial records within a single integrated system. With automated processes and IRAS-ready reporting, companies can reduce manual effort, lower compliance risks, and improve reporting accuracy.

Additionally, ScaleOcean supports scalable tax management through flexible configurations, multi-currency support, and robust internal controls designed for Singapore businesses. Schedule a free demo and explore how ScaleOcean supports accurate, streamlined tax operations.

FAQ:

1. What date is the extra GST payment coming?

The one-time GST/HST credit top-up payment will begin on June 5, 2026. It may still be labeled as the GST/HST credit while banks update their systems. If you have direct deposit, the payment will be credited directly to your bank account.

2. How much is GST in Singapore now?

The current GST rate in Singapore is 9%. GST-registered businesses must charge and account for GST at this rate on all sales of goods and services, unless the sale is zero-rated or exempt under GST law.

3. Will GST in Singapore increase in 2026?

The GST rate remains at 9% in 2026. The last increase was from 8% to 9% on January 1, 2024. Imported goods are also subject to the standard 9% GST rate in Singapore.

4. What are exempt supplies for GST purposes?

Exempt supplies are goods and services not subject to GST, so no tax is charged to customers. Examples include residential property sales or leases, financial services, and investment in precious metals (IPM). Businesses cannot claim input tax credits on expenses related to these supplies.