Accrual accounting is a powerful tool that changes the way companies handle their financial reporting. Instead of waiting for cash transactions, this system records revenues and expenses as they are earned or spent, resulting in a more complete and accurate picture of financial performance.

Accrual accounting helps businesses in Singapore accurately reflect their financial position by recording revenues and expenses when incurred, not when cash changes hands. This aligns with International Financial Reporting Standards (IFRS), ensuring transparency and regulatory compliance.

That focus on accurate reporting matters. According to the data we found from BusinessTime in 2024, Singapore’s accountancy sector grew revenue by 7.5% (S$244.5m), and the Big 4 Deloitte, PwC, EY, and KPMG drove nearly half of that rise. It’s a reminder that accrual records support growth and trust.

By adopting accrual accounting, companies can better track financial performance, make informed decisions, and meet the requirements of local regulations. In this article, we’ll explore the different types of accrual accounting and how they can help businesses manage their finances more effectively.

- Accrual accounting is a great way to record your business’s income and spending when they actually happen, giving you a clearer picture of how well you’re doing financially.

- Using accrual accounting helps make your finances more accurate, improves your planning, ensures you’re following important rules like IFRS, and can actually make managing your cash flow easier!

- If you’re going to switch to implement accrual accounting, it’s important to look at what you’re doing now, make a plan, and get professional help to make sure you get it right.

- ScaleOcean is accounting software that takes the headache out of accrual accounting because it automates your bookkeeping and provides up-to-date financial reports.

What is Accrual Accounting?

Accrual accounting is an accounting method where revenues are recognized when they are earned, and expenses are recorded when they are incurred. This system enables more accurate financial reporting.

It ensures that a company’s true financial condition is captured on its income statement and balance sheet.

Revenue Recognition (recording revenues at the time of sale, not when the cash is received) is a cornerstone of this system. Expense Matching(linking costs to the revenues they generated) is another key principle.

By following these guidelines, accrual accounting provides an exhaustive overview of a company’s finances, thus allowing businesses to make smarter decisions, much like absorption costing, that accurately assign production costs for product costing and inventory value.

How Does Accrual Accounting Function?

Accrual accounting accounts for revenues and expenses when they are earned or incurred, instead of when the cash is exchanged between parties. This helps provide the most accurate and reliable overview of your company’s financial status.

For instance, the income gained for goods or services rendered is recorded when the company performs the service, even though the payment will be received at a later date.

This same principle applies to expenses, as any costs incurred in the company’s name are reported whether or not they are immediately settled.

This method complies with IFRS accounting standards, making the company’s finances consistent and easy to compare with others, and it is particularly helpful for businesses with extended payment terms or high transaction volume.

What are the Types of Accruals?

An accrual account is a method where revenue and expenses are recorded in the income statement and/or balance sheet during the period incurred or earned. There are four basic types:

Accrued Revenues

Accrued revenues are income earned from a business that has yet to be paid by customers. This type of accrual helps the business to accurately report earnings at the time they are earned.

Accrued Expenses

Accrued expenses represent business liabilities that will be paid in the future. These costs must be recognized in the income statement during the period in which they were incurred.

Unearned Revenues

This term is used when payment for services or goods has been received in advance by a business. Under accrual accounting principles, these revenues are recorded in a liability account and recognized when they are earned, as opposed to when they are received.

Prepaid Expenses

Prepaid expenses are funds that have been paid in advance of use. They are recorded on the balance sheet as a current asset and expensed on the income statement over time as the use is enjoyed.

Advantages of Accrual Accounting

Accrual accounting helps businesses by recording expenses when they’re incurred and revenues when they’re earned (not just when cash exchanges hands).

This accounting principle yields a more precise look at a company’s current financial performance, thereby aiding both operational decision-making and ensuring IFRS compliance. The main advantages of this system are as follows:

Enhanced Financial Accuracy

Matching revenues with related costs ensures that business profit is measured with better precision. This system doesn’t rely on the cash balance when determining the amount earned and owed to better display a business’s true financial state.

Improved Strategic Planning

By providing a truer look at performance, accrual accounting enables better future planning, allowing businesses to have more realistic predictions in terms of budget, investment, and strategic choices, aiding overall growth.

Compliance with IFRS

Accrual accounting aligns with International Financial Reporting Standards (IFRS), ensuring business statements can be directly compared with others globally, enhancing credibility. This is vital for companies trading internationally.

As an example of growing trust in accounting, we found data from PeopleMatters in Singapore reported an 8-point rise in the public trust in accountants. This figure increased to 88%, suggesting transparency and accuracy are key for global business operations adhering to IFRS standards.

Better Cash Flow Management

Although it’s mainly focused on revenues and expenses, accrual accounting does assist with predicting future cash flow due to its tracking of both payable and receivable figures on the balance sheet reporting, lessening the chances of unexpected cash flow problems.

Enhanced Stakeholder Trust

Transparent and reliable financials build confidence in your business. It increases trust among investors, creditors, and other stakeholders and demonstrates financial stability to them.

Disadvantages of Accrual Accounting

While the benefits of accrual accounting are evident, there are drawbacks that businesses should be aware of before adopting this system. Key disadvantages of accrual accounting include:

Increased Complexity

Accrual accounting demands more meticulous record-keeping than cash accounting and a deeper knowledge of accounting principles.

Revenue and expense tracking without cash being exchanged requires a greater level of professional understanding and is potentially time-consuming and error-prone.

Potential Cash Flow Challenges

This method emphasizes accrual over cash transactions, so a balance sheet may not truly represent how much cash a business has on hand.

This could create a situation of illiquidity for cash-tight companies, especially considering its impact on the profit and loss statement reports and general ledgers.

Implementation Costs

Switching from cash accounting to accrual reporting may require significant investment in new accounting software and staff training. Smaller firms might find the setup expense to be too steep.

Difficulty in Short-Term Financial Monitoring

It’s often hard to accurately monitor short-term financial conditions with accrual accounting methods, as they primarily focus on the long-term financial health.

This can pose challenges in managing daily operating expenses when solely relying on accrual reports. Using both a bookkeeping spreadsheet and accrual reports provides a dual outlook to monitor cash and general ledger reports better.

Risk of Overstated Revenue

Accrual accounting reports all revenues at the time earned, not necessarily when collected, and this can give misleading expectations of financial status among those with whom the business works, stakeholders, among others.

While a complete financial picture, the setup for accrual accounting can be confusing and costly. It may not be the best option for firms with tight cash flow.

However, ScaleOcean ERP aims to simplify accrual accounting by offering easy-to-use financial reporting software that ensures full visibility into your cash flow and accurately reflects business operations.

Accrual Accounting vs. Cash Basis Accounting

There are two common methods used for maintaining financial records: accrual accounting and cash basis accounting. It is important to know the distinctions between these two accounting systems in order to choose the appropriate one.

Recognition of Revenue and Expenses

In accrual accounting, revenues and expenses are acknowledged when earned or incurred. Income is recognized when a sale takes place, and the time at which the money is received may be.

Likewise with expenses, the cost is acknowledged when the goods or services are received, not when the money is paid.

Conversely, cash basis accounting accounts for revenue and expenses only when cash comes in or goes out. Under this method, business transactions are quickly understood but not necessarily calculated to accurately reflect a company’s financial situation.

Financial Accuracy and Reporting

Accrual accounting provides a more accurate picture of the overall health by enforcing the recording of revenues and any related expenses over the same accounting periods.

This system is particularly useful for larger businesses, such as those that include more complicated systems, such as credit sales, in their daily accounting cycles.

Conversely, although cash basis accounting provides a simple picture of the cash flow statement reports, it does not depict the true nature of the ongoing financial performance by excluding all outstanding receivables and payables.

Compliance and Suitability

Accrual accounting is a must if you have to follow the international accounting standards (like the International Financial Reporting Standards (IFRS)), and this is usually the case for large companies or companies raising external funds.

Although it is used by many SMEs or sole traders, cash basis accounting is quite simple and easy to implement. It is not IFRS-compliant, though.

Complexity and Resource Requirements

Accrual accounting is more complex, requiring detailed record-keeping and a thorough understanding of accounting principles. It often involves advanced software and professional expertise, making it resource-intensive.

In contrast, cash basis accounting is easier to manage and requires fewer resources, making it ideal for small businesses with limited accounting requirements.

Cash Flow Visibility

Accrual accounting gives a far more accurate representation of the financial performance as a whole, but does not give an accurate indication of cash flow, as this takes into account all unpaid invoices and expenses.

This is why it is also important to look at a financial leverage example. Cash basis accounting, on the other hand, applies only to cash movements, providing a more up-to-date short-term financial position.

Implementing Accrual Accounting in Singapore

Accrual Accounting is an essential business practice in Singapore to be compliant and for correct financial reporting. This document provides an overview of regulations and how to implement accrual accounting in Singapore.

Utilizing accounting software can also help make this transition easier, as it can automate many processes and save you time.

1. Regulatory Framework

Both businesses and sole traders are required to use accrual accounting and must comply with the Singapore Financial Reporting Standards (SFRS).

The SFRS states that all financial reporting should be transparent and compared with other businesses and sole traders.

Being compliant not only meets legal requirements but also encourages stakeholders, investors, and regulatory agencies.

2. Transition Process

There are three major steps to this conversion: first, reviewing existing accounting procedures to evaluate current baselines, then mapping out an implementation plan with specific timelines and resource commitment, and finally undertaking the change process with external help.

Using techniques such as double-entry accounting in such a manner can help ensure the balance and accuracy of records. This method provides a structured form of process that minimizes undue disruptions and provides a smooth transition to accrual method reporting.

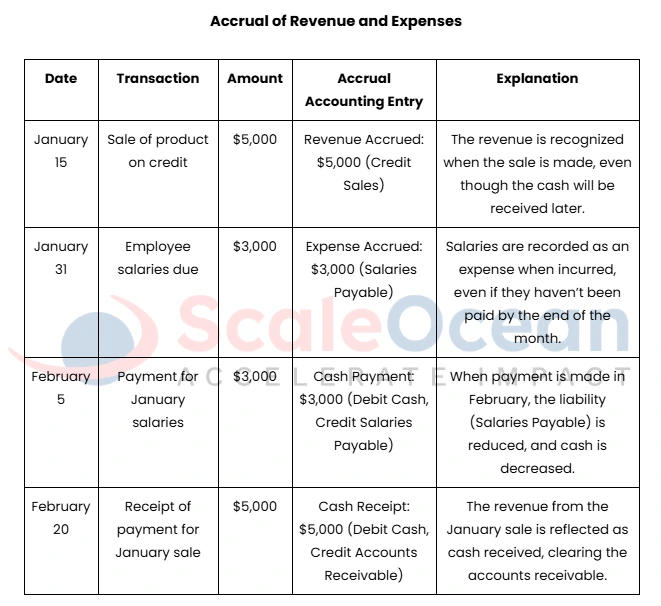

3. Example

Here is a sample “accrual accounting ” calculation using “business financial accounts”. Here we look at the accumulation of revenue and expenditure.

Example: In January, a firm provides goods to its customer on credit and records the sale immediately. Work goes on in January, and wages accrue but are paid in February, so the expense is recognized in January, and the payment in February just clears the accrued balance in payroll.

Explanation:

Revenue Accrued: This is the income earned when the product is sold on credit instead of when the actual payment is received for that product. This entry ensures that the report shows the real income statement examples.

Expense Accrued: The salaries expense is booked as and when due, even if the payment has not been received. The expense related to the period.

Payment Made: The cash account is credited when February’s cash is paid in for January’s (since the payment clears the liability)

Cash Receipt: Any payment received in January for a sale will decrease the Receivables and increase cash to illustrate the receipt of cash.

Efficient Bookkeeping Strategies with Accrual Accounting

The adoption of accrual accounting in business necessitates organized bookkeeping procedures to stay on top of the business ledgers and make the best business decisions.

Key bookkeeping practices, such as reconciliation, employee education, and the utilization of accounting software, are summarized in this guide. Here are the key strategies for efficient bookkeeping:

Regular Reconciliation

Reconciliation of accounts is an important aspect of financial management. Accounts have to be reconciled regularly while being updated.

Managing bookkeeping and accounting professionally would make sure that there is regular reconciliation of accounts and that those published reflect proper inflows and outflows in the accounting period in accordance with Singapore Financial Reporting Standards (SFRS).

This type of practice also helps to early error detection, which leads to superior financial transparency.

Employee Training

Accrual accounting should be taught to employees. Training should include efforts in understanding the SFRS, identifying accruals, and best practices.

Well-trained staff can perform complex transactions with ease, avoiding costly errors.

Utilize Comprehensive Accounting Software

A robust accounting system is vital, and for Singapore companies, one of the best software solutions is ScaleOcean. If you are seeking a solution that fits SFRS requirements and uses it within the company, then ScaleOcean offers a custom accounting system designed for accrual accounting.

These solutions assist businesses in keeping their books. Additionally, ScaleOcean’s accounting software has features to automate the financial aspect of the business and is able to interact with other financial modules of the software to keep efficient accounts of all transactions.

In addition, all payroll and expenses of ScaleOcean are automatically included within the CTC grant, making it a hassle-free solution to your payroll requirements while maintaining best accounting practices.

See for yourself the benefits of automated and compliant payroll by requesting a free demo.

Key Features:

- Automated Journal Entries: Simplifies the recording of accruals and deferrals, reducing manual intervention.

- Real-Time Financial Reporting: Provides up-to-date financial statements that support informed decision-making and enhance transparency.

- Compliance Assurance: Ensures adherence to Singapore’s accounting standards, helping businesses maintain regulatory compliance.

- Automated Reconciliation: Automatically matches transaction data recorded in the company’s system with bank records, reducing manual errors.

ScaleOcean Accounting Software helps you work smarter by decreasing the time required for manual data input, which also reduces human error.

The scalable nature ensures the system grows with your business’s financial requirements. The easy-to-use system can be used by your entire workforce, improving overall performance and sharing workload.

No matter if you are a start-up or a large enterprise, ScaleOcean provides precise and easy handling of the accounting function. Furthermore, the system can be configured to local legislation.

Conclusion

Accrual is one of the most important accounting policies to accurately state the financial position of an organization and is also compliant with the applicable accounting standards in Singapore. While it has its own limitations, its benefits cannot be denied.

To streamline and expedite, we can rely on modern accounting software, e.g., ScaleOcean, that helps to automate the process of accrual accounting. ScaleOcean can directly feed the data to journal entries and reports, automate reconciliations, and minimize the risk of mistakes.

Works perfectly without interrupting your business operations, providing real-time financial information and accounts continuity. ScaleOcean accounting software provides businesses with simple and reliable financial management and ensures compliance with current regulations.

FAQ:

1. What is the basic rule for accrual accounting?

Accrual basis accounting combines two key accounting principles: the matching principle and the revenue recognition principle. This means that revenues and expenses are recorded when earned or incurred, not when cash transactions occur.

2. Is accrual a liability or an asset?

Accruals are liabilities to pay for goods or services that have been received or supplied but have not been paid, invoiced, or formally agreed with the supplier, including amounts due to employees (e.g., accrued vacation pay).

3. What are the three steps to accrue an expense?

You record an accrued expense journal entry by debiting the expense account and crediting a liability account. This entry reflects the cost your business has incurred but not yet paid or invoiced. These expenses are recorded in three steps: the initial recognition, the reversal, and the payment.

4. Which assets are excluded from accruals?

1. An Inheritance: Property passing at the owner’s death to the heir or to those entitled to succeed.

2. A legacy: An amount of money or property left to someone in a will.

3. Donation: An instance of presenting something as a gift or contribution.